Block Part Two: Square

A turnaround is possible, but significant work remains

Disclosure: I do not hold a position in Block. I am long Global Payments, Shift4 Payments, and Fiserv, mentioned in this article. I hold no position in other companies mentioned.

The Big Picture

Square pioneered payment acceptance by introducing the dongle, allowing smartphone users to process card payments. Alongside innovative technology, Square disrupted traditional merchant acquiring with a single, transparent price.

Next, Square launched a point-of-sale system integrating payments with proprietary hardware and software, later adding features and customized solutions for restaurants, retailers, and service-based businesses.

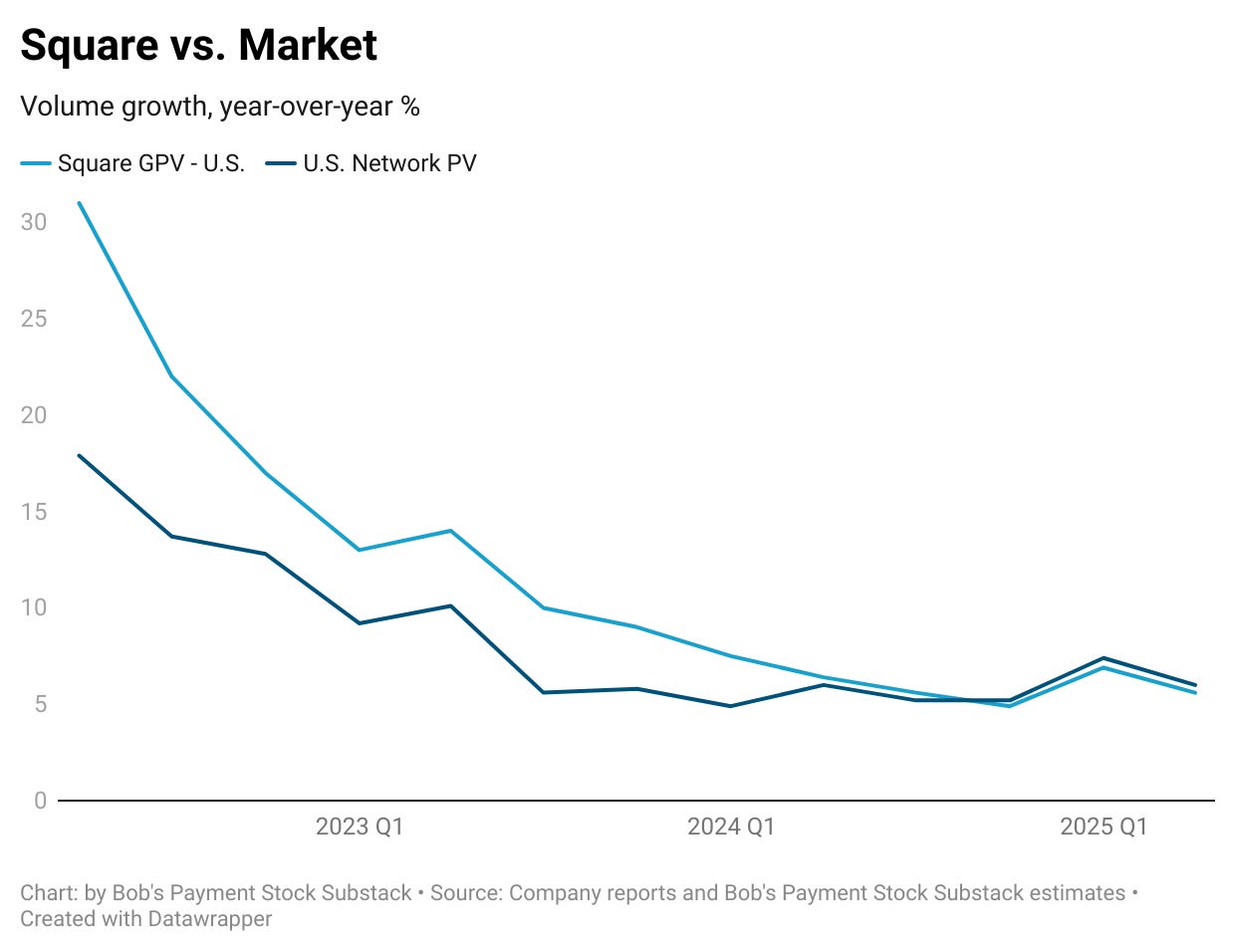

Square maintained efficient distribution through word-of-mouth marketing, keeping customer acquisition costs low and payback periods short. But after years of strong gains, Square's U.S. GPV growth is converging with the market.

Facing intense competition, Square aims to boost growth by adding new features and expanding distribution. The opportunity for integrated payments internationally is vast, and Square has shown early, sustained success.

The bottom line: Although much work is ahead, I'm optimistic about Square's turnaround potential due to its trusted brand and developer competency. However, renewed growth may be costly. Efficient distribution is likely ending, and investments in expanded commerce features, sales, and partner models may limit profitable growth. Approximately 80% of Square’s gross profit comes from spending-based or recurring sources, emphasizing Block’s need to accelerate Square’s growth to offset Cash App’s increased lending mix.

Tale of the Tape

Square faces numerous competitors, including the processing arms of major banks like J.P. Morgan, Bank of America, Wells Fargo, and U.S. Bank, as well as Global Payments, which recently agreed to acquire Worldpay. All vie aggressively for small merchants.

The following companies, similar to Square, integrate processing capabilities into proprietary software for small businesses in discretionary spending categories, such as restaurants, retail, entertainment, and hospitality.

The Players

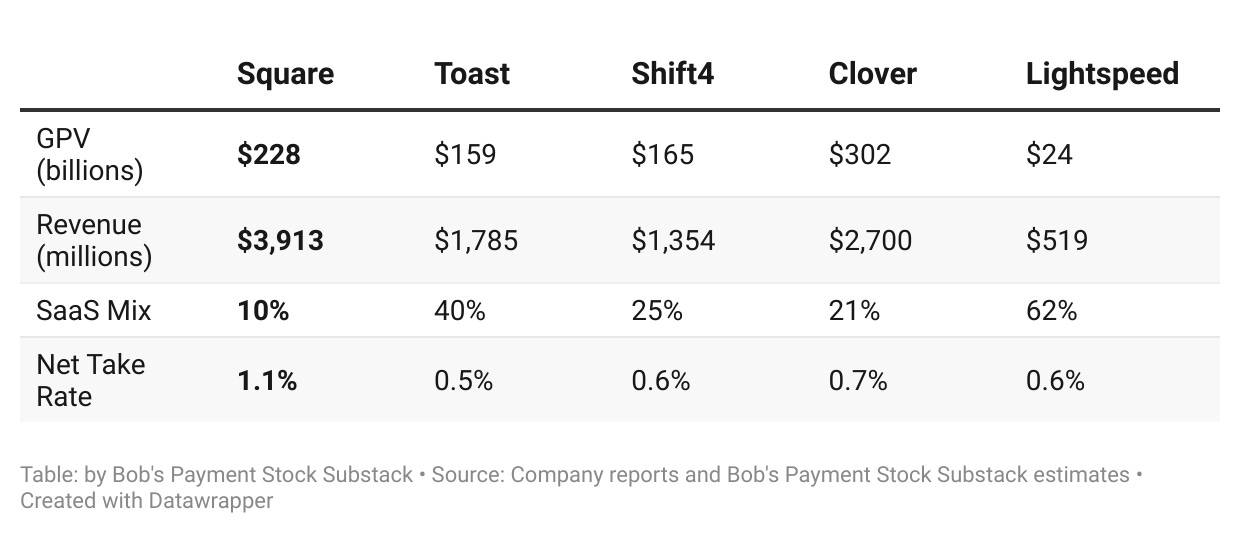

Toast serves upscale restaurants with a unified commerce platform and strong local sales presence, driving top-tier growth. In the latest period, Toast’s locations, volume, and revenue grew 26%, 25%, and 34%, respectively. Toast’s plan to move down market may challenge Square’s core business in food and drink, which made up 33% of Square GPV during 2024.

Shift4 integrates its processing and third parties into various software platforms via its proprietary gateway, streamlining payments for complex businesses like resorts with hotels, restaurants, spas, retail stores, and golf courses. Its SkyTab software serves upscale restaurants, bars, hotels, and stadiums.

Clover, Fiserv’s platform for small businesses, integrates payments with proprietary hardware, software, and third-party apps. It leverages Fiserv’s distribution channels, including direct sales, financial institutions, and partner organizations.

Lightspeed offers commerce platforms for restaurants and retailers. Formed through multiple software acquisitions, it aims to expand its processing capabilities into a substantial gross transaction volume opportunity.

Moats in Payments

Payments companies offer attractive investment opportunities. The industry benefits from secular growth, and many firms have built moats around their businesses to protect long-term profits.

Moat sources include networks, scale, diverse and efficient distribution, and owned software integration. Let’s take a look at each for Square.

Networks. Unlike most competitors, Block leverages a two-sided network of cardholders and merchants for Cash App Pay. It's too early to determine if this will provide a long-term advantage for Square and Cash App, but other acquirers with similar capabilities have seen limited success. Verdict: Developing

Scale. Although Square handles significant volume, it is dwarfed by the largest merchant acquirers. Additionally, Block depends on processors where pricing is fixed, even as transactions rise. Verdict: No

Diverse Distribution. Square's reliance on direct and word-of-mouth marketing limited its distribution. Its decision to establish a field sales presence and form partnerships will diversify distribution, boosting customer acquisition. Verdict: Developing

Efficient Distribution. For years, Square benefited from efficient distribution through word-of-mouth marketing, driving organic customer growth at little cost. We believe rising competition hinders Square’s ability to maintain this efficiency, particularly among larger merchants they target. Thus, the need to expand distribution. Verdict: Yes, but Weakening

Software Integration. Square sits at the sweet spot of payments: providing processing solutions to small businesses through integration with owned software. Combining processing, hardware and software boosts customer retention and revenue yield. Verdict: Yes, and Strengthening

Square: A Payments Tool Evolving into a Commerce Platform Distributed through Multiple Channels

Square is transitioning from a payments tool with added features to a unified commerce platform for small businesses with integrated payments.

Square is investing in field sales and forming partnerships to boost distribution of its unified commerce platform, targeting vertical-specific, horizontal, and third-party sales organizations.

Square expects its enhanced commerce platform to boost retention and wider distribution to speed up customer acquisition, driving improved volume growth during 2025.

Square believes it is regaining market share in key categories and maintaining attractive payback periods despite increased investments.

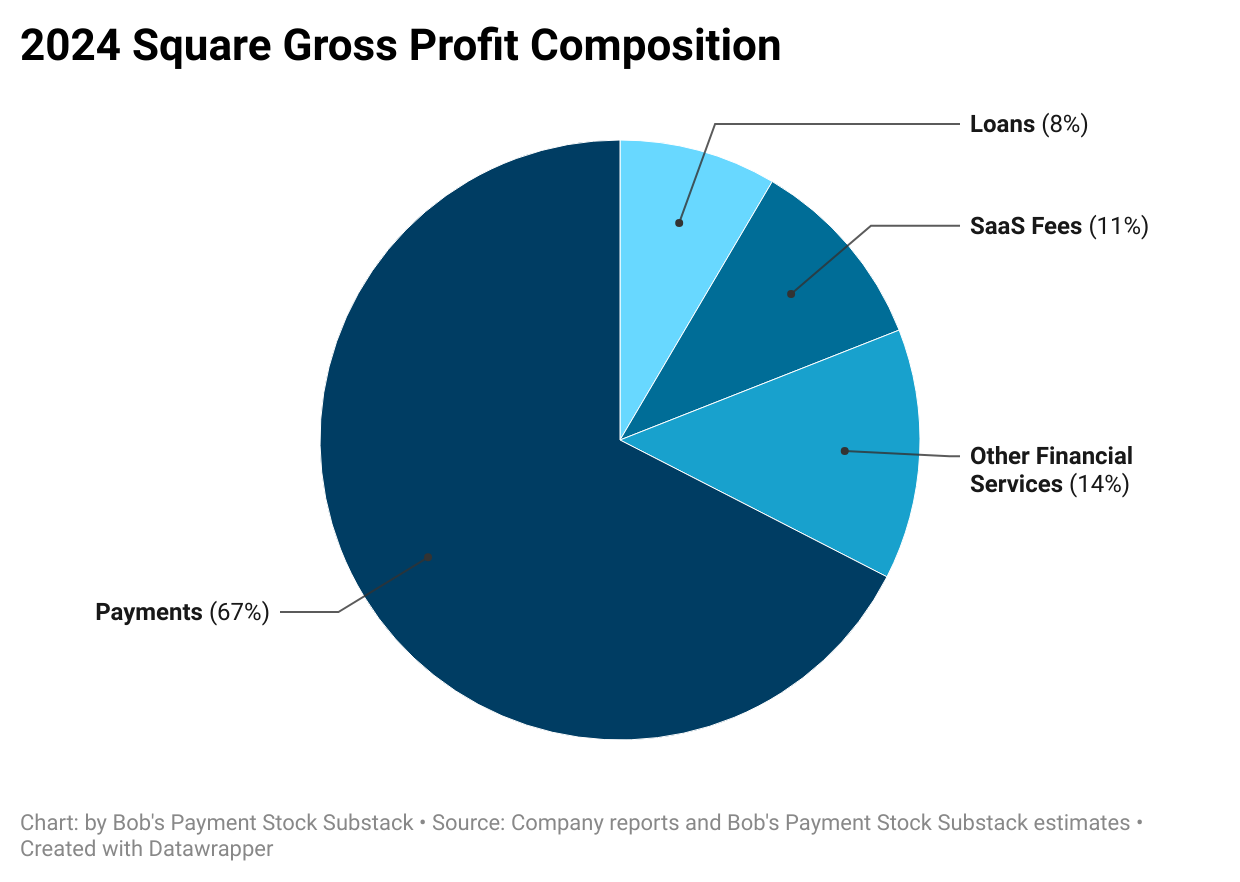

Payments ($2.5 billion or 67% of 2024 gross profit): Square earns fees from merchants for payment processing, including a percentage of the transaction value plus a small per-transaction fee. Square collects merchant fees, pays interchange and processing costs, and retains the difference as its net take rate, estimated at 1.1% during 2024. Net take rate varies by merchant size, with larger merchants receiving custom pricing, and transaction funding type, as credit cards have higher interchange rates than debit cards.

Other Financial Services ($0.5 billion or 14% of 2024 gross profit): Square's other financial services include the Square Debit Card and instant transfers. Square earns interchange revenue from Square Debit Card spending and a 1.75% fee on instant transfers.

SaaS Fees ($0.4 billion or 11% of 2024 gross profit): Square earns subscription fees from its point-of-sale systems and features like payroll and customer relationship management. Most systems and features offer a free basic tier, with advanced options available for an additional cost.

Loans ($0.3 billion or 8% of 2024 gross profit): Square offers loans to merchants, repaid by withholding a percentage of processing volume. Square either sells or retains these loans as investments. I assume the loans' gross profit is 5.5% of the $5.7 billion origination volume in 2024.

Square Gross Profit: Mostly Best

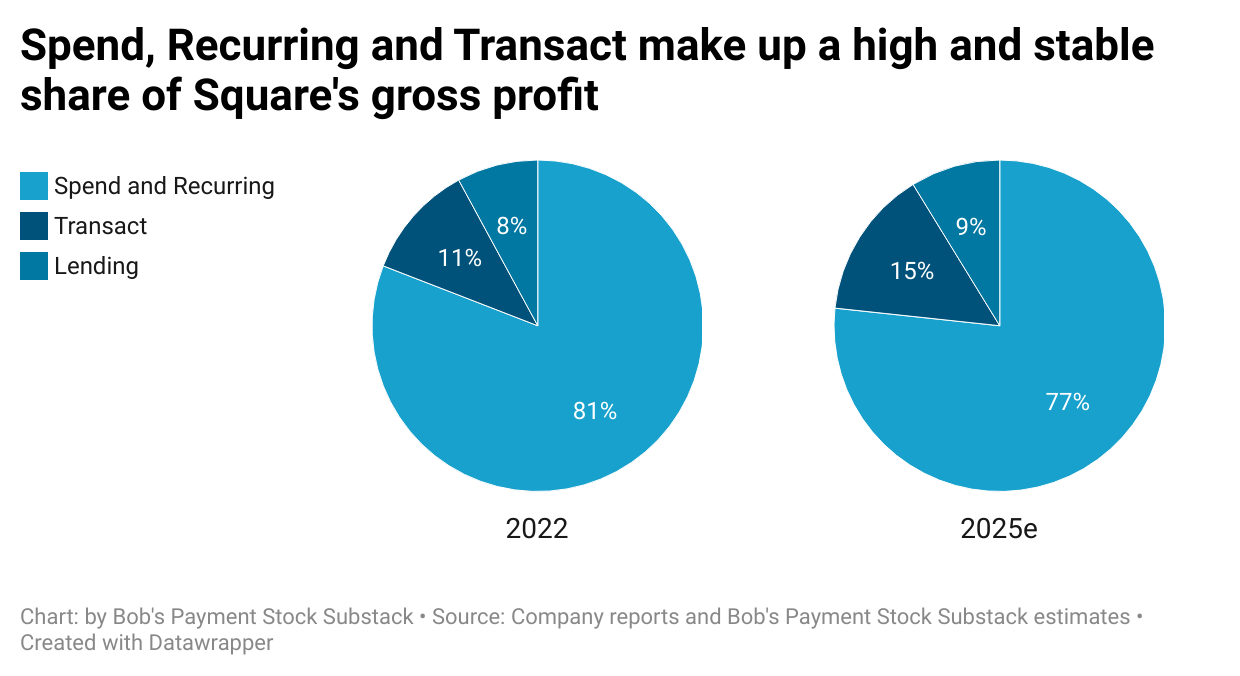

Like Cash App, I separate Square’s gross profit into three categories: good, better, and best. Unlike Cash App, most of Square’s gross profit comes from the best sources.

The good, which I refer to as Lending includes gross profit from Square Loans. Lending can be influenced by risk tolerance and incur losses on the back end.

The better, which I refer to as Transact, includes gross profit from instant transfers and interchange. I consider interchange from the Square Debit Card the best but cannot confidently determine its precise amount.

The best, which I refer to as Spend and Recurring, includes gross profit from payment processing and SaaS fees. It is the most predictable but has grown slower than Square’s total gross profit.

For 2025, I estimate Square GPV will grow in the high single digits with a stable net take rate, SaaS fees will rise in the low double digits, Square Loan originations will increase by the mid-teens, and financial services gross profit, including from instant transfers and the Square Debit Card, will expand the fastest.

Putting it Altogether

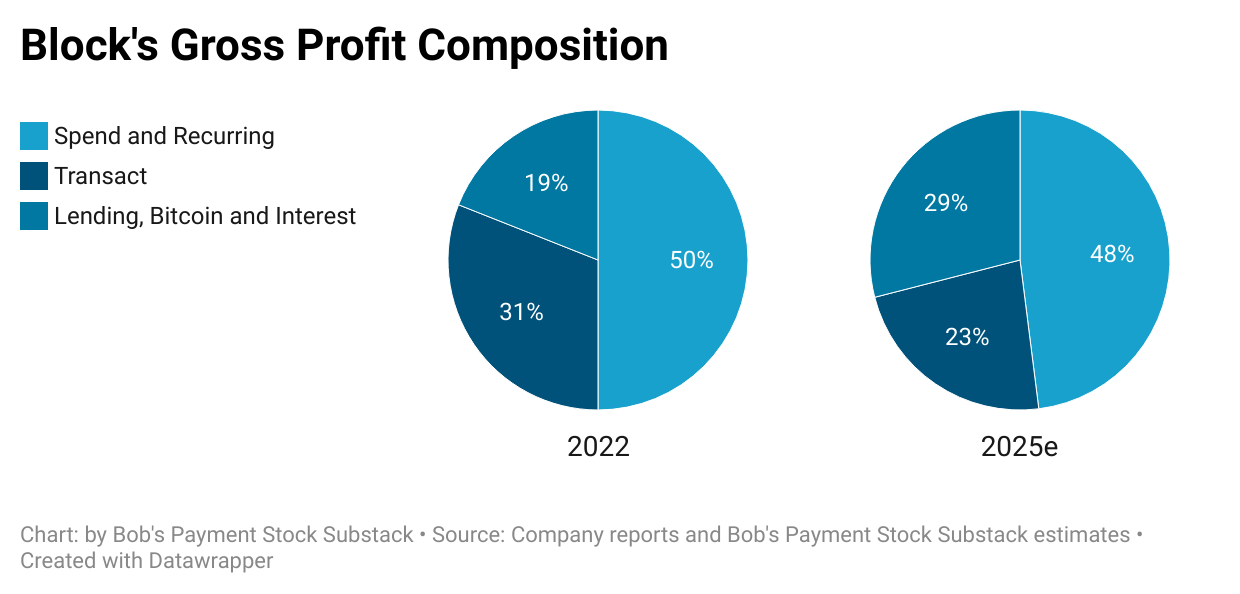

In 2025, I estimate 71% of Block’s gross profit will come from the best sources - Spend, Recurring, and Transact - down from 81% in 2022. Meanwhile, gross profit from Lending, Bitcoin, and Interest is expected to rise from 19% to 29%.

For Block’s multiple to expand, it must accelerate Cash App Card monthly actives and spend, Square U.S. merchants and GPV, and Square subscription fees. Without this, less valuable streams will increasingly dilute the gross profit mix and multiple.