Chime Financial

Unhappily Ever After?

Investment Brief

In the year since its IPO, Chime’s execution has been solid. It is thoughtfully monetizing its member base to drive attractive top-line growth while maintaining a sizable cost advantage relative to incumbent banks and other fintechs, leveraging ChimeCore—its proprietary processing platform and ledger system, which was delivered ahead of schedule—to innovate faster and lower costs, and moving toward meaningful GAAP profitability sooner-than-expected. Still, shares have languished, down about one-third from their IPO price of $27. I believe there are a handful of contributing factors:

Total spending-based volume growth is slowing. In its latest quarter, Chime’s total spending-based volume, which includes card purchases and outbound instant transfers, or OITs, grew 14.5%, slowing from more than 19% growth at the start of 2025. This is a continuation of a longer-term trend that has seen Chime’s spending-based volume growth fall below active member growth, suggesting fewer active members are adopting Chime as their primary financial relationship, which is defined as a member that has made at least 15 card purchases or received one qualifying direct deposit of $200 in the past calendar month:

At the time of its IPO, the company reported 67% of its active members used Chime as their primary financial relationship, driving 55 transactions per month, on average, across its member base. Although Chime has not updated these metrics, their language has shifted…slightly. Now, a ‘majority’ of members use Chime as their primary financial relationship, driving ‘more than 50’ transactions per month, on average, across its member base. While the change may sound trivial, minor changes in the trajectory of Chime’s most important KPI—primary financial relationships—can be meaningful for a fast-growing, and high-multiple company, like Chime.

Lending-based revenue is becoming a larger part of Chime’s business. As of Q2 2024, lending-based contributions to Chime’s revenue were minimal. Now, they make up about 20%. By the end of 2026, with the planned expansion of Instant Loans, they could make up closer to one-quarter of Chime’s revenue. While lending products are important, and a key reason why some members join Chime, the market places a lower value on their associated revenue and profit, in my opinion. Overall, slowing spending-based volume growth and an increasing mix of lending-based revenue is generally not a good combination, and was particularly problematic for Block’s Cash App. I believe spending-based volume growth must stabilize or improve before shares of Chime can move materially higher.

Competition is increasing. Chime faces a range of competitors: incumbent banks, domestic fintechs like Cash App, Venmo, SoFi, Dave, MoneyLion, now owned by Gen Digital, OnePay by Walmart, Green Dot, and Netspend, BNPL providers like Affirm and Klarna, and global fintech heavyweights like Nubank and Revolut. Although not dramatically different, in my opinion, an argument can be made competition is increasing. By Chime’s own admission, since SpotMe, Chime’s fee-free overdraft product, was launched in 2019 banks in the United States have cut overdraft fees in half. Given that avoiding fees is one of the main reasons why a new member joins Chime, lower—or zero—overdraft fees at incumbent banks may make it less likely people switch. Among domestic fintechs, incentives are on the rise as they all chase the coveted direct deposit relationship. Launched in November 2025, Cash App Green provides similar benefits—a higher savings rate, special rewards, and higher borrowing limits—as Chime Plus to entice greater engagement. Likewise, Venmo is offering enhanced rewards (5% cash back) at select brands when a user direct deposits $500 into their Venmo account each calendar month. Both Affirm and Klarna offer a card that can flex between everyday spend funded by a checking account and BNPL loans for larger discretionary purchases. Finally, Nubank and Revolut have applied for bank charters in the United States and promise a concerted effort to expand in the country if (once) approved.

Macro is concerning…always. Many fintechs suffer from perpetual caution on the low-to-middle income American consumers they serve. Thus far, the group has held up in the face of sustained high inflation as the labor market—despite a few bumps—and wage growth remain healthy. Although Chime argues the company may benefit during difficult times due to its low cost leadership, the market is concerned about a further slowdown in spending, elevated credit losses, or a lack of originations that may occur during an economic downturn.

Thoughts on the Stock. From my perspective, Chime is among the most consumer-friendly fintechs in the world, which should stand for something. What I believe it provides Chime is greater visibility into sustained revenue growth of 15-20% and substantial progress on reaching the company’s long-term adjusted EBITDA margin goal of 35%, or more. At less than 16x my 2027 EBITDA estimate of $409 million, which is burdened for stock-based compensation, Chime starts to look attractive. However, to borrow a biblical phrase, there is no room left at the inn given an abundance of higher-quality payment and fintech companies trading at, what I believe, are similarly attractive valuations. While Chime is a name to consider for gaining exposure to fintech lending, I still prefer Block over Chime, and the best values I see today across payments and fintech—and where I’m allocating capital—are Mastercard, Intuit, Adyen, and Broadridge Financial, in no particular order.

Highlights

Low cost provider. Chime lives up to its motto of being free where possible and offering the lowest cost product when fees are necessary. Like most other fintechs, Chime offers fee-free checking, debit card, and overdraft, a better deal relative to incumbent banks. For lending, where fees are necessary to compensate for losses, Chime offers the lowest cost product among fintechs. For MyPay loans—which can be free if members wait 24 hours to receive funds—Chime’s yield was 2.6% in Q1 2026, significantly below Dave’s 6.4% yield on ExtraCash advances. Although Block does not disclose its revenue from Cash App Borrow, it charges a 5% flat fee per loan and may assess late fees and accrue interest on past due balances, suggesting a yield of up to 6% or more. For installment loans, both Affirm and Klarna charge up to a 36% annual percentage rate, or APR. Based on data from Affirm, I estimate the average APR on their outstanding installment loans is 30%. Although details are still emerging, it appears Chime may earn fees equating to an APR in the mid-to-high teens on their Instant Loans, suggesting a sizable discount to Affirm. How does Chime do it? First, Chime’s privileged repayment position, backed by recurring direct deposits, results in industry-leading loss rates, allowing Chime to generate healthy transaction margin on the lowest cost product. Second, ChimeCore provides a unique cost advantage for Chime, contributing to its ability to be the low cost provider while generating attractive consolidated profitability.

Monetization runway. Given the daylight between Chime’s pricing on lending products and other fintechs, there is significant runway for Chime to improve monetization while remaining the clear low-cost provider, an enviable position, in my opinion. The best example: I expect Chime to originate $18.6 billion of MyPay loans during 2026. If instead of generating a yield of 2.6%, Chime earns…say…4%—still significantly below competitors—it would result in an additional $250 million of revenue for Chime at (theoretically) zero incremental cost. Chime is monetizing in other ways that brings value to both itself and members. By moving new and existing members’ spend to a secured credit card, which functions nearly identically to a debit card, members are able to establish or improve credit and earn rewards while Chime generates higher interchange fees. Chime believes its secured credit card will be a long-term revenue tailwind. In addition to monetizing existing spending and lending, Chime plans to introduce new products, like investment accounts, that should contribute modestly to average revenue per active member, or ARPAM, growth over time.

Proprietary technology systems. Chime boasts owning 100% of its tech stack, including ChimeCore, its proprietary processing platform and ledger system. This reduces Chime’s cost to serve. The conversion to ChimeCore reduced processing costs by 60%, contributing to Chime’s ability to maintain a low-cost advantage. It also allows Chime to develop and launch products faster and in a proprietary way, as working with a third-party may result in innovation being spread among competitors. Finally, having access and visibility into 100% of its data should help Chime develop leading AI-powered tools for internal use and members.

Strong balance sheet. Chime has no debt and approximately $1 billion of cash and short-term marketable securities, providing flexibility to acquire companies and capabilities, or return money to shareholders through buybacks and potentially dividends.

Risks

In addition to increasing competition and macro concerns discussed above, Chime faces the following risks:

Durbin carveout. Even though Chime is among the largest issuers of debit cards by purchase volume in the United States, it benefits from an exemption to the debit interchange cap, imposed by the Durbin Amendment, meant for smaller banks. As a result, Chime generates hundreds of millions of dollars of revenue that could theoretically be eliminated if the spirit of the law is followed. Potentially mitigating this risk is Chime’s decision to steer new and existing members to the Chime Card, a secured credit card, which generates higher interchange and is on firmer regulatory ground.

Credit exposure. Chime’s direct deposit relationships give them a privileged repayment position, limiting losses on SpotMe and MyPay loans, which are repaid in less than two weeks. However, Chime appears set to move more aggressively into higher value installment loans that span up to 12 month repayment terms, exposing Chime to more significant losses if there is a downturn in the economy, or a slowdown that disproportionately impacts its mainstream American member base.

Banking license may prompt shift away from asset-light model and result in lower multiple. At a recent conference, Chime indicated that its decision to apply for a banking charter is a matter of when, not if. While moving away from an asset-light partner model to being a bank may bring certain benefits, it could tie up more of Chime’s capital and depress its multiple as the company’s earnings power matures.

Too stingy? Although Chime deserves credit for its low-risk lending strategy, it may miss opportunities to acquire or retain customers by bringing loss rates down too low. Although Chime has mentioned testing a different version of MyPay for non-direct deposit members, it does not appear to have gone anywhere.

Business Overview

Chime offers a range of financial services to the hundreds of millions of mainstream Americans making less than $100,000 per year. Chime is not a bank (yet), so it relies on partners (Stride Bank and The Bancorp Bank) to hold deposits, issue cards, and make loans, while Chime manages the technology infrastructure and user experience. Given its digital-only footprint, Chime’s cost to serve is dramatically lower than the branch model employed by traditional banks, allowing Chime to offer free or lower-cost solutions. Approximately 90% of Chime’s new members are unhappily banked by the large incumbents like Bank of America, J.P. Morgan, and Wells Fargo. Although Chime spends significantly on advertising ($510M in 2025), approximately half of its new members come from word-of-mouth marketing and referrals from existing members, driving attractive customer acquisition costs, or CAC, relative to lifetime value, or LTV. Historically, Chime focused on acquiring members that will make Chime their primary financial relationship immediately. However, at around the beginning of 2025, Chime altered its strategy to make it easier for customers to interact with more of their products before making a full-fledged primary financial relationship commitment to Chime.

Chime’s most significant products are as follows:

Checking. An FDIC-insured checking account with no monthly fees, no minimum monthly balance requirement, and access to 47,000 fee-free ATMs nationwide. Members can receive their scheduled direct deposits two days early with Chime’s Get Paid Early feature. Although Chime pioneered this capability several years ago, most major banks now offer it. Chime generates revenue from spending on debit cards attached to the checking account and from fees for out-of-network ATM withdrawals.

Overdraft. Chime allows certain members to overdraft up to $200 fee-free on debit, credit, and ATM transactions. Members must be enrolled in either Chime Plus or Chime Prime to access SpotMe. Chime does not charge for SpotMe but instead relies on optional tipping. For those members not enrolled in SpotMe, transactions that exceed the existing balance are declined. Loss rates on SpotMe loans are less than 0.4%.

P2P. Chime’s Pay Anyone feature allows members to send money instantly to both Chime and non-Chime members for free.

Outbound Instant Transfers. Chime began offering OITs in 2025. Instead of pulling money into another app or account from Chime, which could take a few days and would be monetized as debit card purchase volume, OITs allow members to instantly push money for a 1.75% fee.

Savings. Chime offers different interest rates on members’ savings balances depending on their level of engagement with Chime. For members that do not qualify for a premium tier, Chime currently pays 0.75%. For Chime’s most premium tier, Chime Prime, which requires $3,000 of monthly direct deposits, Chime currently pays 3.75% on savings balances, several times the national average. Chime holds members’ saving balances in a sweep account at one of its partner banks and recognizes revenue based on the spread between what it earns and what it pays out to members.

Secured Credit Card. A secured credit card functions like a debit card in the sense that members pre-fund an account before making purchases. Unlike a debit card, using a secured credit card can build credit history or improve an existing score. Also, given higher interchange rates on secured credit card purchase volume, members have access to greater rewards potential by spending with a secured credit card. Last year, Chime introduced the Chime Card, its latest secured credit card. Prior to launch, credit represented 16% of Chime’s total card purchase volume. In March, credit represented nearly 25% of total card purchase volume with Chime noting that over half of new members are adopting the Chime Card and those members using it for 70-80% of their total spend. Chime Card volume generates 175-bps of interchange, net of rewards. With the launch of Chime Prime, which offers 5% cash back on a rotating category selected by the member, Chime expects rewards costs to increase in the coming quarters.

MyPay. Members with a qualifying direct deposit can access up to $500 of their paycheck for free if they wait 24 hours, or instantly for a fee of 3%, with a minimum fee of $2 and a maximum fee of $5. Previously, Chime charged a flat $2 fee for an instant MyPay loan. The average MyPay loan is $85 and is repaid in less than 2 weeks. From its full launch in July 2024, Chime has originated $25 billion in MyPay loans and loss rates have fallen from 170-bps to 100-bps, which Chime believes will be MyPay’s steady state loss rate.

Instant Loans. Members with a qualifying direct deposit can access a 3-to-12 month installment loan for up to $1,000. Chime charges a flat fee of $5 to $20 per loan, which is added to the principal and repaid ratably over a monthly basis. Since its launch in March of 2025, Chime has originated $580 million of Instant Loans. The average Instant Loan size and term is $250 and 6 months, respectively. Loss rates are currently around 4% but loss rates for repeat borrowers fall by half.

Chime offers special perks to members who make qualifying direct deposits:

Chime Plus: With a single $200 direct deposit or a cumulative $400 in direct deposits over the last 34 days, members are eligible for Chime Plus, which offers access to SpotMe, Chime’s fee-free overdraft product, a 3% savings rate, 2% cash back on up to $1,500 of spending per month with the Chime Card on a rotating category chosen by the member, and priority 24/7 member support.

Chime Prime. With at least $3,000 in direct deposits over the last 34 days, members are eligible for Chime Prime, which offers access to SpotMe, Chime’s fee-free overdraft product, a 3.75% savings rate, 5% cash back on up to $1,500 of spending per month with the Chime Card on a rotating category chosen by the member, and priority 24/7 member support.

Chime Workplace: Chime’s newest distribution channel is Workplace for enterprise customers. Its free for employers, and employees can access 100% of their paycheck on a daily basis for free due to the minimal losses Chime incurs given their direct integration with an employer’s payroll system. Chime monetizes the relationship by capturing employees’ everyday spend. Customer acquisition costs are significantly lower for Workplace and while Chime believes it will be a long-term driver of member growth, enterprise sales cycles are long, so investors should temper their expectations over the near-term.

Corporate History

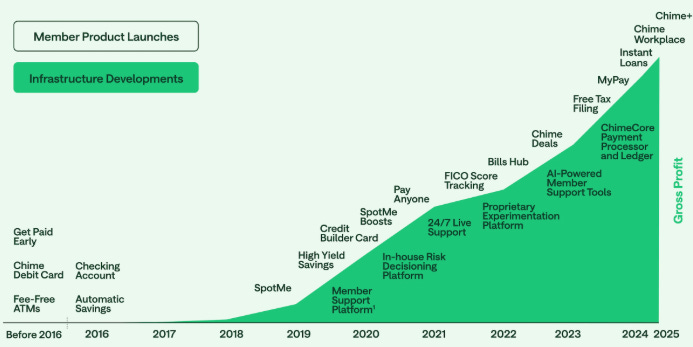

Chime was co-founded by San Francisco neighbors Chriss Britt and Ryan King in 2012. Britt (current CEO of Chime), formerly of Visa and Green Dot, was focused on the business side, while King (current CTO of Chime), a former head of engineering at a startup, was tasked with developing the technical aspects of Chime. Since its launch in 2014, Chime has evolved from a simple prepaid card to a holistic digital financial services platform for mainstream Americans:

No fintech story would be complete without mentioning the heights Chime reached (on paper) during 2021, when it was valued at $25 billion in a funding round led by Sequoia Capital. Chime entered the public markets almost exactly one year ago. The company’s IPO price of $27 implied a market cap of $11-12 billion. On an intraday basis, Chime’s all-time high market cap reached more than $19 billion. Fast forward to today and Chime’s market cap of approximately $7 billion is a far cry from its past glory.

Chime has made few acquisitions throughout its history with the most recent being Salt Labs in 2024 (for up to $173 million, based on earnouts), a company focused on daily earned wage access, the nexus of Chime Workplace, the company’s enterprise channel.

Chime has a dual-class share structure, giving Britt and King nearly 75% of voting power and effective control over Chime.

Strategy

Chime’s strategy is relatively straightforward: acquire direct deposit relationships by offering free or the lowest cost products, monetize primarily through everyday spending, and attach additional products that generate revenue for Chime and bring value to its members.

Chime relies on word-of-mouth marketing, referrals, and paid media to acquire members. Word-of-mouth marketing and referrals account for about half of new members acquired. Total customer acquisition costs, which include advertising, brand marketing, referral bonuses, and other marketing incentives, ranged from $93 to $130 per customer acquired on a quarterly basis since 2022, with Q1 2026 coming in at $107. Given the long-lasting nature of direct deposit relationships, which can last 10-15 years, Chime’s LTV to CAC is attractive at 8x or more, translating to a payback period of 5-6 quarters currently, down from approximately 7 quarters one year ago.

Chime’s pace of innovation has accelerated with the launch of Instant Loans, the Chime Card, Workplace, and Chime Prime, all in the past year or so. Over the remainder of 2026, Chime plans to introduce new checking account options, including joint and custodial accounts, rollout investing features, including support for Trump Accounts, and launch Jade, its AI co-pilot for members. Over the long-term, Chime plans to launch products in support of its highest-earning members, its fastest growing category. Among the products mentioned is an unsecured credit card.

Members that attach 6 products or more make up 15% of Chime’s total active members, up from just 5% two years ago. ARPAM for these members is greater than $500, more than double Chime’s average.

Workplace represents a significant opportunity for long-term, low-cost member growth. Although rollouts among the small number of employers that have signed up are going well, Chime has stressed the enterprise channel will not be a material contributor to growth over the near-term as sales cycles are long.

Financial Review and Estimates

For 2026 and 2027, I estimate revenue of $2,699 and $3,179 million, implying growth of 23% and 18%, respectively:

Key assumptions:

I expect card purchase volume growth to slow to approximately 12% in 2026 and 2027.

Credit will represent 31% of total card purchase volume by Q4 2027.

Including OITs, total spending-based volume growth is estimated to be 14.6% and 14.0% in 2026 and 2027, respectively.

Spending-based revenue is expected to grow 18.7% in 2026, down 220-bps from 2025, better than the 340-bps decline in volume growth, as more volume shifts to higher-yielding credit and OITs, offset by a moderate decline in the credit net interchange rate due to increased rewards costs. For 2027, I expect spending-based revenue growth of 17.5%, down 120-bps.

I expect MyPay originations of $18.5 and $21.7 billion during 2026 and 2027, respectively.

I assume a yield on MyPay originations of 2.64% and 2.75% in 2026 and 2027, respectively, reflecting little-to-no change in the product’s current pricing schedule.

I assume OIT volume of $5.9 and $9.5 billion in 2026 and 2027 with OIT revenue of $104 and $166 million, respectively, reflecting consistent pricing of 1.75%.

Admittedly, Instant Loans are a bit of a wildcard and dependent on Chime’s preferred pace of originations, which influences revenue and loss rates. For 2026, I assume Instant Loan originations of $960 million, with a quarterly cadence of $180, $220, $260, and $300 million. In 2027, I expect originations of $1.42 billion. In order to derive revenue, I take a rolling three quarter average of originations, multiply by two to reflect a 6 month average duration and multiply this average outstanding balance estimate by 4.25% to reflect an APR of about 17%. Based on this framework, I arrive at Instant Loans revenue of $72 and $111 million in 2026 and 2027, respectively. This, of course, could be dramatically different if Chime ramps up originations more significantly and my understanding of the product’s APR is off-base.

Remaining other revenue reflects ATM fees—which I expect to grow moderately slower than active member growth—and various other categories including tips on SpotMe loans, excess savings revenue, referral fees, and fees for facilitating cash deposits. The decline in other revenue in 2026 and 2027 primarily reflects the impact of lower interest rates on Chime’s excess savings revenue.

For 2026 and 2027, I expect adjusted EBITDA of $449 and $694 million, implying a margin of 16.6% and 21.8%, respectively. On an incremental basis, this translates to a low-60 percent margin in 2026, above Chime’s guidance for the mid-50s percent. My estimate for 2027 implies an incremental margin in the low-50s percent:

Gross profit, exclusive of depreciation and amortization, is expected to be 89.5% in 2026 and nearly 90% in 2027.

I expect transaction and risk losses as a percentage of revenue to be above 14% in 2026 and 2027, reflecting an uptick from Q1 2026 as MyPay loss rates have likely bottomed and Chime ramps up Instant Loan originations, which carry higher loss rates.

For cash operating expense, excluding transaction and risk losses, I assume 13% growth in 2026, up about 2-points from 2025, followed by 8% growth during 2027.

I assume stock-based compensation of $271 and $285 million in 2026 and 2027, representing 10% and 9% of revenue, respectively.

As always, thank you for reading, and if you’ve enjoyed this, please consider sharing, liking, commenting or subscribing!

Disclosure: As of June 14, 2026, of the stocks mentioned in this report and across payments and fintech, I am long Visa, Global Payments, Intuit, Block, Adyen, Shift4 Payments, Paychex, Mastercard, and Broadridge Financial. This report is for informational purposes only and is not a recommendation to buy or sell any stock. Finally, while I rely on the information in this report to guide my investment decisions, you should not, because I cannot guarantee its accuracy.