Fiserv Investor Day Notes

Retention, Clover, Modernization + AI, Financial Outlook

Fiserv hosted an investor day last Thursday (May 14). Here are my notes from the presentation:

Retention. Fiserv relies on cross-selling to grow revenue (boost average revenue per client), improve margins (additional revenue comes on at high incremental margins), and increase its value to clients (relationships become stickier when more products and services are taken). Retaining clients as a base for cross-selling is critical to Fiserv’s strategy. New management is taking several steps to improve retention: rolling back excessive price increases, using AI to quickly resolve basic service inquiries, adding frontline personnel to increase client coverage, and making investments to improve technology and systems resiliency.

Attrition has been most acute within Fiserv’s core banking franchise where platform consolidations and service gaps have doubled attrition rates (versus its historic baseline) over the past few years. According to Fiserv, every $1 of core processing revenue generates an additional $2.70 of revenue from an average of 10 other products and services across Fiserv’s Financial Solutions segment. With $1.3B of core processing revenue in 2025, this implies total revenue of $4.8B from core clients, half the segment’s total. During 2023-2025, core and related revenue attrition represented 1.5-points of total Financial Solutions revenue, implying $142MM for 2025, or 3% of core and related revenue. I’m uncertain if this is just voluntary attrition or includes involuntary attrition (clients being acquired by banks with non-Fiserv cores). Either way, this is a low number (even if it has doubled over its historic baseline) and demonstrates the attractiveness of Fiserv’s core banking franchise. Fiserv believes its actions to date (no forced conversions, $142MM invested in stability and operations, and its Smith Consulting Group acquisition) are starting to ‘bend the curve’ on core platform attrition. Still, Fiserv is not forecasting a quick return to historical levels, but rather a gradual decline, reaching its historical baseline by 2029, an appropriately prudent assumption and one of the reasons why Fiserv is forecasting banking revenue to grow at the lower-end or below its 2-4% medium-term outlook for the Financial Solutions segment.

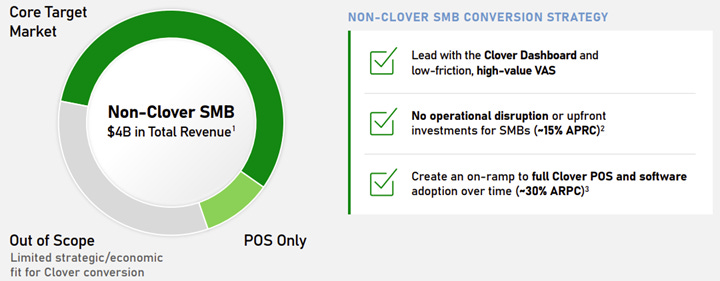

Non-Clover SMBs. Even though Clover is among the largest commerce platforms (a POS system combining hardware, software, and processing), non-Clover SMBs still generate $4B of revenue (1.8MM locations and $700B of GPV), greater than the $3.3B of Clover revenue. Much like its strategy in core banking, Fiserv does not intend to force non-Clover merchants to convert to Clover. Instead, Fiserv will support non-Clover SMB solutions and offer high value Clover upgrades that result in minimal disruption for a non-Clover merchant: the Clover dashboard, Clover Capital, Clover Savings, and its new marketing agent. Fiserv believes this package will result in a revenue uplift of 15%. Converting a non-Clover merchant to the full Clover experience will result in a 30% revenue uplift. Fiserv estimates 50-60% of its $4B of non-Clover SMB revenue is in scope for upgrade or conversion. An uplift of 15% on this base equals $330MM of revenue with the full conversion generating $660MM of additional revenue, or about 6.5% of total 2025 Merchant Solutions revenue:

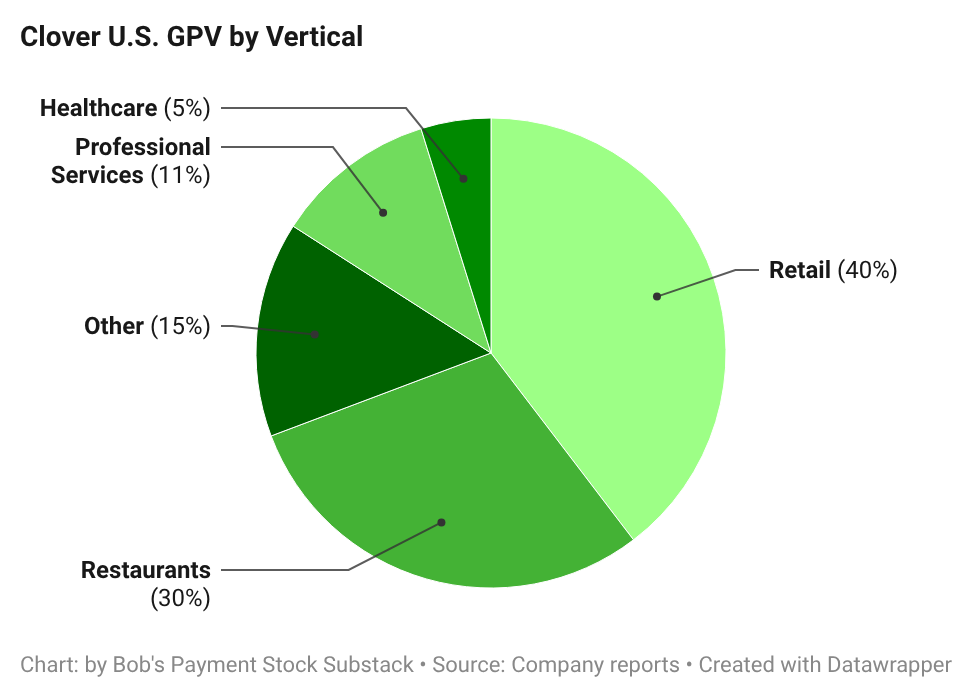

Clover Details. Fiserv had 910k Clover merchants at the end of 2025, up from ~700k at the end of 2023. Clover merchants generate $357k in GPV per location compared to $53k for Square (based on 4.5MM sellers) and $1,189k for Toast. Excluding value-added services (VAS), Clover’s revenue of $2.47B (2025) represented 76-bps of GPV, which compares to a payments take rate of ~107-bps for Square, ~49-bps for Toast, and ~60-bps for Shift4 Payments. Clover’s non-VAS revenue includes hardware sales, which are unknown. In the Merchant Solutions segment, product revenue (which is likely the best proxy for hardware sales) represented 12.5% of total revenue during 2025. Assuming a similar contribution to Clover, implies payments revenue of $2.08B, or 63-bps of GPV. After re-reading the Q1 earnings call transcript, even though implied non-VAS Clover revenue grew LSD, Fiserv stated Clover’s payment processing revenue grew 10%, more in-line with reported GPV growth (9%), suggesting a stable payments take rate, and a more significant decline in hardware sales. Unlike Square and Toast, Fiserv generates an ‘appropriate and stable operating margin’ from Clover hardware sales. Only $30B, or approximately 9%, of Clover’s total GPV is online. Here is my estimate of Clover’s U.S. GPV composition based on Fiserv’s disclosures:

Restaurants. Restaurants are an important category for payments companies. It’s a big market (food services and drinking places generated $1.18T in retail sales in 2025) with surprisingly durable growth and lots of SMBs, presenting attractive revenue opportunities from software penetration (moving restaurants to cloud-based POS systems) and payment processing (higher take rates). Clover, Toast, Square, Shift4, and Global Payments are all major players in restaurants. According to Fiserv, Clover’s U.S. restaurant GPV grew at 4x the cumulative industry rate from 2023 to 2025, a surprisingly strong showing despite a resurgence at Square, Clover’s formidable competitor in limited-service restaurants. It’s not entirely clear what industry growth rate Fiserv refers to. According to the U.S. Census Bureau, from 2023 to 2025, retail sales at food services and drinking places increased slightly less than 11% in total. If we use limited-service eating places, the increase was 8.5% in total. Both aggregate enterprise customers and SMBs (and Fiserv may be referring to a proprietary SMB growth rate). If we use the 8.5% increase for limited-service eating places as the industry growth rate, this implies 34% growth (4 x 8.5%) for Clover’s U.S. restaurant GPV, lower than Toast’s 55% increase, but more than 31% for Square. The natural question is: if Clover, Square, and Toast are all gaining significant ground in restaurants, who’s losing? The answer is likely the long-tail of smaller, less robust restaurant POS systems, legacy on-premise providers, and non-Clover Fiserv.

ISVs. An interesting part of Fiserv’s strategy with Clover is developing highly specialized vertical-specific solutions in partnership with ISVs. Historically, payments companies embed only processing capabilities within ISVs, earning limited economics. Fiserv’s new strategy combines most Clover capabilities (hardware, VAS, and processing) with vertical-specific software from ISVs, creating a potentially best-in-class commerce solution and allowing Fiserv to keep more economics, a win-win for all parties. The first iteration of this strategy was the launch of Clover PracticePay for healthcare providers last summer. PracticePay combines the practice management software of Rectangle Health with Clover’s commerce capabilities. Last week, in a similar fashion, Fiserv announced Clover Reserve powered by Tabit for full-service and fine dining restaurants. Fiserv plans additional ISV partnerships.

Modernization + AI. Like other payment and fintech companies, Fiserv is leaning heavily on AI to create better solutions (faster) and lower costs by automating certain business functions, including customer service and software development. In the category of easier said than done, Fiserv believes its collection of assets (although dispersed) and the corresponding data it creates will be significantly enhanced by AI, allowing Fiserv to catch-up to competitors…but not be disrupted by new entrants using the same AI tools. I found this portion of the presentation to be particularly ambitious:

“But what excites me the most is the intersection of AI and data which allows us to move beyond moving money to understanding identity. We start with the incredible scale of Fiserv across all of our businesses, more than 100 billion transactions plus everything that we know about them from the FI side of the business that Dhivya will cover later. These are then aggregated to individual consumer and small business profiles which gives us a very deep understanding of the vast majority of U.S. consumers and businesses.

And then to that, we have behavioral information through partners like Signifyd that capture pre- and post-sale signals, how people browse, how often do they return or dispute, for example. And then we embed those into a graph neural network that we developed in collaboration with NVIDIA, which resulted in a significant increase in the accuracy of our models and that we just deployed in production. Of course, all of that comes with robust data governance.

That gives us an incredibly detailed and real-time view of how consumers and businesses behave across the economy. This, we believe, will shift us over time from a bulk transaction processor that earns basis points on the dollar to an intelligent platform that earns percentage points on the dollar, unlocking entirely new revenue pools and making us true partners to our clients. You can see some of the examples on the right, and we are going to go through many of them later. This means more volume, new products and higher take rates for us as well as more revenues and better customer experience for our clients.”

Takis Georgakopoulos, Co-President, Merchant Solutions at Fiserv Investor Day

Fiserv highlighted the following modernization and AI efforts:

Launching an enhanced omni-channel payments platform for enterprise and platform customers early next year featuring new customer identification tools, fraud controls, routing optimization, embedded finance solutions, and payouts. If successful, it would rival modern offerings from Adyen, Stripe and Braintree.

Updates to its card issuing platforms Optis and VisionNext. Optis is for larger traditional card issuers, while VisionNext is Fiserv’s cloud-based platform for modern use cases that will compete with companies like Marqeta and Pismo. Fiserv highlighted a $250MM pipeline for VisionNext with four implementations already in flight.

Fiserv is launching agentOS in collaboration with OpenAI for its financial institution customers. agentOS will offer a marketplace of agents that complete tasks across Fiserv’s banking platforms. The marketplace will include agents built by Fiserv and third-parties as well as the tools for banks to build agents themselves.

Financial Outlook. There was little surprise in Fiserv’s medium-term outlook (2026-2029) relative to what the company shared last October when it reset its financial baseline: 4-6% adjusted revenue growth (total not organic, but contemplates no significant M&A), more than 300-bps of cumulative margin expansion (50-bps annually from operating leverage and 200-bps from Project Elevate savings), a majority of FCF directed to share buyback, and double-digit EPS growth.

By segment, Fiserv expects 6-8% adjusted revenue growth for Merchant Solutions, and 2-4% growth for Financial Solutions:

Within Merchant Solutions, Fiserv expects Clover revenue to grow 15-20% and enterprise growth to be in the MSDs. Clover revenue growth will be boosted by increased penetration of VAS, including Capital (which is used by only 4.5% of Clover merchants), and conversion of non-Clover SMBs to Clover. The remaining portion of Merchant Solutions, which makes up approximately half of current segment revenue, is expected to be relatively flat.

For Financial Solutions, banking is expected to be at the low-end or slightly below the broader segment goal of 2-4% growth with issuing and digital payments at the higher-end of the range.

FCF conversion is expected to be 90% with capital expenditures averaging 8% of revenue over the medium-term outlook. The tax rate of 21-22% is higher than the 19% it has averaged over the past few years. Fiserv expects 2029 EPS to be above $12, implying a CAGR of nearly 14%.

Here is my outlook for 2026-2029 along with my Fiserv model:

As always, thank you for reading, and if you’ve enjoyed this, please consider sharing, liking, commenting or subscribing!

Disclosure: As of May 17, 2026, of the stocks mentioned in this report, I am long Global Payments, Adyen, Block, and Shift4 Payments. This report is for informational purposes only and is not a recommendation to buy or sell any stock. Finally, while I rely on the information in this report to guide my investment decisions, you should not, because I cannot guarantee its accuracy.