Long Zoetis (ZTS)

The global leader in animal health is on sale

My Positioning in Animal Health

I made an initial investment in Zoetis during early 2025 after valuation moved to a reasonable level. With recent purchases, I now own 300 shares of Zoetis, about 3% of my portfolio. In addition to Zoetis, I own shares of IDEXX Labs, reflecting my favorable view of the animal health market. Of the two, and especially after the highly favorable reaction to IDEXX’s Q2 earnings, I believe Zoetis possess a more favorable risk-reward profile. Zoetis reports tomorrow (8/5) and, no, this is not a prediction that earnings will be either good or bad.

Investment Thesis

I believe the market has an overly negative view of the impact from new products on Zoetis’ leading position in parasiticides and dermatology, while underestimating the untapped potential of these markets, the attractiveness of animal health overall, and Zoetis’ ability to create and lead billion-dollar animal health categories in the future.

Parasiticides and dermatology are key growth areas for Zoetis, but face increased competition

In 2024, Zoetis’ key parasiticide and dermatology products, Simparica, Apoquel and Cytopoint, accounted for one-third of the company’s total revenue and grew 22%. Recent product launches in these categories include:

Elanco’s Credelio Quattro (January 2025) and Merck Animal Health’s Bravecto Quantum (July 2025) will compete with Zoetis’ Simparica Trio in triple combination parasiticides.

Elanco’s Zenrelia (September 2024) and Merck Animal Health’s Numelvi (July 2025, in the EU) will challenge Zoetis’ dominance in dermatology.

Although the company’s guidance incorporates the potential for some slowing in organic revenue growth in the second half of 2025 from these new products, I believe the impact will be moderate and temporary because:

Zoetis enjoys first-mover advantage and high customer satisfaction, making it unlikely many pet owners will switch products without a clearly superior efficacy profile, which these new products lack, in my opinion.

The introduction of competing products has the potential to accelerate category growth as increased marketing spend raises consumer awareness of new treatment options.

There remains significant untapped potential in parasiticides and dermatology

Of the 90 million dogs in the United States, only one-third are treated for fleas, ticks, and heartworm. Of those 30 million treated, only one-third use a triple combination product. Zoetis expects the triple combination market to more than double over the next 4 years, reaching $4.5 billion during 2028.

While Zoetis treats 12 million dogs with its dermatology products, 20 million more dogs have dermatology issues and see a vet but are untreated by Zoetis’ products. Plus, many of the 12 million dogs treated with Zoetis’ dermatology products lack full compliance, presenting an opportunity for Zoetis.

The animal health market remains highly attractive

Putting aside any near-term impact from increased competition in parasiticides and dermatology, the animal health market has several favorable characteristics, and Zoetis should benefit long-term from:

Rising pet ownership, longer pet lifespans, and increased spending on pets.

Consistent pet spending, even during recessions.

Growing demand for animal protein from a rising global population.

A larger number of cash-paying customers, supporting industry pricing power, unlike human-focused pharmaceuticals that have fewer large payers, including governments, insurers and pharmacy benefit managers.

Shorter development periods, less regulatory scrutiny and limited competition from generics.

Zoetis' history of creating and leading large animal health categories bodes well for future opportunities in pain management, chronic kidney disease, and oncology

Zoetis has several important advantages over competitors:

Independence from a human-focused pharmaceutical company enables Zoetis to develop products solely for animals' unmet needs.

An industry-leading research and development engine, with investments split between expanding existing products and creating new ones.

Longstanding veterinarian relationships and trusted brands among pet owners.

The company is targeting three new large opportunities: pain management, chronic kidney disease and oncology. In each instance, Zoetis is pursuing a market unserved by a specialized animal health product.

In pain management, Zoetis launched monoclonal antibody treatments for osteoarthritis in dogs and cats, generating $581 million in revenue during 2024, with an expected peak of over $1 billion. Of the 27 million dogs with osteoarthritis in the U.S., Zoetis reports 1.2 million are treated with Librela, 8 million with NSAIDs, and about 18 million remain untreated.

Zoetis anticipates approvals for its monoclonal antibody treatments for oncology and chronic kidney disease among dogs within 1-3 years. The company estimates the chronic kidney disease market could generate over $3 billion annually in revenue and the oncology market up to $2 billion.

Risks

Zoetis faces the following risks:

Zoetis' ten largest products generated 55% of total revenue in 2024. Adverse developments for any one of those products could negatively impact the company’s financial performance.

Investments in inventory and capital expenditures have reduced Zoetis' free cash flow below non-GAAP net profit for years.

Tariffs on pharmaceuticals may raise Zoetis' costs, limiting the company’s profitability or requiring additional price increases.

The new administration's focus on reducing drug costs could affect Zoetis or perceptions of its impact.

Growing resistance to animal protein treated with vaccines or antibiotics may decrease the demand for Zoetis' livestock products.

Zoetis' pipeline may not yield new blockbusters, or competitors could reach the market first.

Librela, Zoetis' monoclonal antibody for dog osteoarthritis, has faced negative publicity, potentially limiting its potential.

Valuation

Zoetis trades at 23.4x the next twelve-month consensus EPS estimate, a notable discount to the company’s 3-year, 5-year, and 10-year averages.

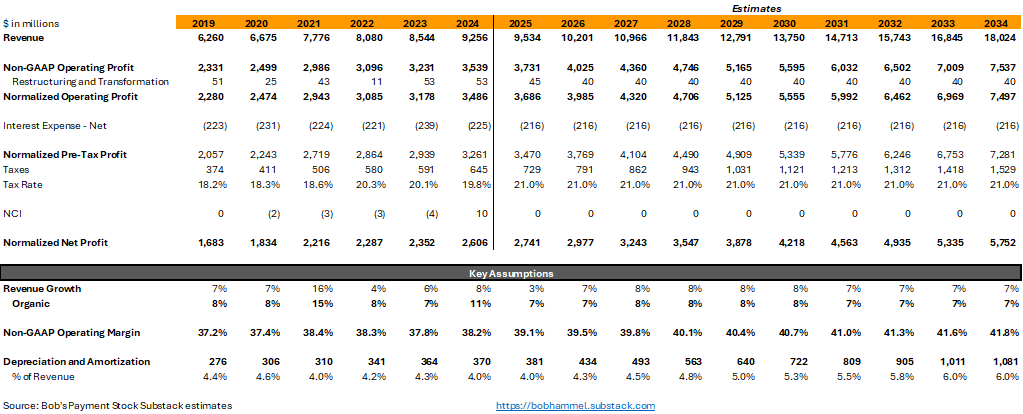

My fair value of nearly $170 implies a multiple of 26x the next twelve-month consensus EPS estimate, still a discount to the company’s long-term averages. The key assumptions for my DCF model are:

Organic revenue growth averages 7.3% over my 10-year forecast. While roughly in the middle of the company’s 6-8% medium-term range, it’s below the company’s average of nearly 9% over the past decade. Underpinning my estimate is Zoetis growing a few points faster than market growth in the mid-single-digits.

Non-GAAP operating margin expanding from 38.2% to 41.8% over my 10-year forecast. Zoetis should continue to maintain pricing power, especially as monoclonal antibodies account for a greater percentage of revenue, facilitating an expansion in profitability.

A tax rate of 21%.

I assume capital spending remains high for the next two years before returning to its long-term average of about 6% of revenue over the rest of my forecast period. Accordingly, I assume depreciation and amortization, excluding acquired intangible assets, rises from 4% in 2024 to 6% of revenue by the end of my 10-year forecast.

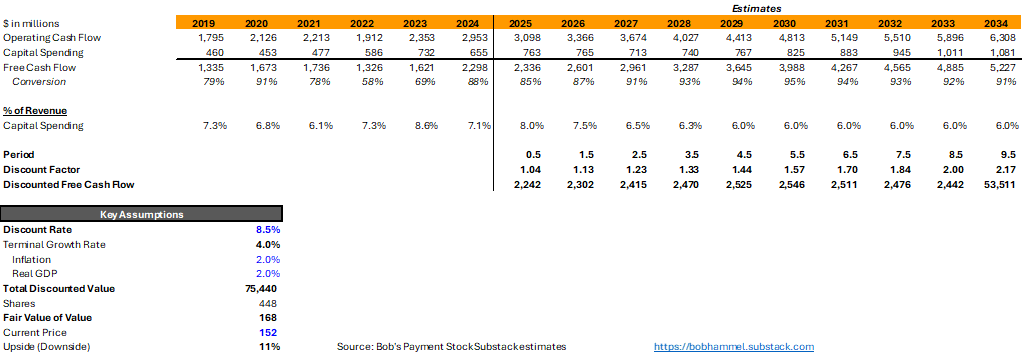

Free cash flow conversion that averages 91% of net profit.

An 8.5% discount rate, which I believe is appropriate given the stability and growth potential of the animal health market and Zoetis’ reasonable financial profile.

Discount rate sensitivity. All else being equal, increasing my discount rate to 9% would reduce Zoetis’ fair value to $151, essentially the current share price, while moving the discount rate down to 8% would increase my fair value to $190, implying upside of about 25%.

Company Overview

Zoetis discovers, develops, manufactures, and sells medications, vaccines, and diagnostics for companion animals and livestock. The company offers over 300 product lines, including 17 blockbusters, which Zoetis defines as generating more than $100 million in annual sales. Zoetis maintains leading positions in dermatology (anti-itch treatments), parasiticides (for fleas and ticks), and pain management. More than half of the company's revenue is generated from outside of the United States, with products for dogs and cats accounting for roughly two-thirds of overall business.

The company's origins date back to the 1950s when Pfizer scientists developed Terramycin, an antibiotic for livestock. Pfizer subsequently expanded its Animal Health division through several acquisitions, notably the purchase of SmithKline Beecham’s animal health business in 1995, which facilitated entry into the companion animal market. In 2013, Pfizer spun off its Animal Health division under the name Zoetis. Since becoming independent, Zoetis has continued making strategic acquisitions, further broadening its presence in companion animals, including an expansion into diagnostics.

Key Products

Zoetis separates its products into the following categories:

Parasiticides treat fleas, ticks and worms.

Vaccines prevent diseases.

Dermatology relieves itching associated with allergies and skin conditions.

Anti-infectives kill bacteria, fungi or protozoa.

Pain and sedation alleviate pain associated with osteoarthritis.

Other pharmaceuticals include antiemetic (helps with nausea and vomiting), reproductive and oncology.

Diagnostics analyze blood, urine and other animal samples.

Zoetis’ top five products accounted for 41% of revenue in 2024, and the top 10 selling products contributed 55% of 2024 revenue.

The Animal Health Market and Competitors

Although many companies compete in the animal health market, the largest five account for a significant percentage of total revenue. They are Zoetis, Merck Animal Health, Boehringer Ingelheim Animal Health, Elanco and IDEXX Labs, which specializes exclusively in diagnostics.

Since 2017, I estimate the market1 grew at a compound annual rate of 6.3%, with Zoetis growing about 3 points faster.

In the beginning, all animal health businesses were part of human-focused pharmaceutical companies. Pfizer spun-off Zoetis in 2013 and Eli Lilly spun-off Elanco in 2018. Merck Animal Health remains part of Merck and Boehringer Ingelheim Animal Health remains part of Boehringer Ingelheim, a German pharmaceutical.

Together, Zoetis, Merck Animal Health, Boehringer Ingelheim Animal Health, Elanco and IDEXX Labs reported about $29 billion of revenue in 2024 with Zoetis accounting for about one-third of the total.

Unlike its competitors, with the exception of IDEXX Labs, Zoetis generates more than two-thirds of its revenue from companion animals, while Merck Animal Health and Elanco report more revenue from livestock than companion animals.

Financial Overview

Below is an evaluation of Zoetis using my Investing Checklist.

Disclosure

Zoetis discloses revenue by species, geography and product category. The company provides further disclosure of revenue by key product lines, including Simparica, Apoquel, Cytopoint, Librela and Solensia. Importantly, the company consistently discloses organic revenue growth and the contribution from volume and pricing. The company reports earnings on a non-GAAP basis, adding back non-recurring items, acquisition-related costs, and amortization of acquired intangible assets.

Growth

Over the past decade, Zoetis’ organic revenue growth averaged nearly 9% with volume contributing about 6 points of growth and pricing 3 points. Growth has been incredibly consistent, ranging from 7% to 15%.

Zoetis sells its products to veterinarians, distributors, livestock producers and directly to pet owners through retail and e-commerce outlets. In 2024, the company’s largest U.S. veterinary distributor accounted for 14% of Zoetis’ revenue.

Profitability

Over the past decade, Zoetis significantly boosted profitability, with its adjusted operating margin rising from under 25% in 2014 to over 38% in 2024. Margin growth slowed over the last five years, increasing by about 100 basis points since 2019.

Free Cash Flow

Over the past decade, Zoetis converted only 76% of its non-GAAP net profit to free cash flow, indicating low earnings quality due to high capital spending and increasing inventory days. Zoetis aims to improve free cash flow by streamlining inventory and reducing capital spending to its historical 6.5% range. This is my primary concern, and in my 10-year forecast, I assume free cash flow conversion averages 91%, better than the past decade but below 100%.

Financial Health

As of March 31, 2025, Zoetis had $6.58 billion of debt versus $1.72 billion of cash and short-term investments, implying a net debt-to-EBITDA ratio of 1.7x, a reasonable level, in my opinion. All long-term debt was at fixed rates with coupons of 2.0%–5.4% and maturities from 2025 to 2050.

Returns

Over the past decade, Zoetis' returns on average tangible assets ranged from 24% to 42%, with 2024 at 35%. In 2024, the company's return on average capital was 25%.

Capital Allocation

Over the past decade, Zoetis repurchased $7.9 billion of its shares, reducing the share count by 9.5%. It increased its per-share dividend at a 22% compound annual rate, with the payout ratio rising from 15% to 29%. Since 2015, Zoetis spent $3.85 billion on acquisitions, including $2 billion for Abraxis, a diagnostic equipment specialist, in 2018.

Disclosure: Of the stocks mentioned in this report, I am long Zoetis and IDEXX Labs. I do not hold a position in any of the other stocks mentioned in this report. This report is for informational purposes only and is not a recommendation to buy or sell any stock. Finally, while I rely on the information in this report to guide my investment decisions, you should not, because I cannot guarantee its accuracy.

I define as aggregate organic revenue growth for Zoetis, Merck Animal Health, Boehringer Ingelheim Animal Health, Elanco and IDEXX Labs

Thanks for the analysis. I am wondering why analysts have recently downgraded ZTS and upgraded ELAN. I have seen that ELAN is gaining market share, but the balance sheet is still concerning to me. Thus, I would prefer ZTS

Very nice, thanks for sharing this analysis. Very clean as well. Zoetis is in my watch list in balance for a potential entry - in competion with TMO/GMAB. I already have MRK and will as the cycle pharma cycle begins.