A deep dive on the new Global Payments

Added complexity and heightened execution risk overshadows the potential strategic benefits of combining Global Payments and Worldpay

Disclosure: I am long Global Payments. I hold no position in any of the other stocks mentioned in this article.

The Big Picture

Global Payments believes a combination with Worldpay will create a formidable player in merchant acquiring. One with significant scale, diverse customers and distribution, a global footprint, and extensive capabilities. Investors are skeptical.

The bear case. Both Global and Worldpay are in the midst of big changes. The outcomes are uncertain, and success is far from guaranteed. Any individual progress may take a step back during an integration. Worse, even if things go smoothly, investors wonder if the new Global will have the tools to win.

The bull case. The bar is extremely low. Global trades at an absurd valuation (6x 25E EPS of $12.10). Survival feels like success. Any improvement and the stock may rip.

Key Findings

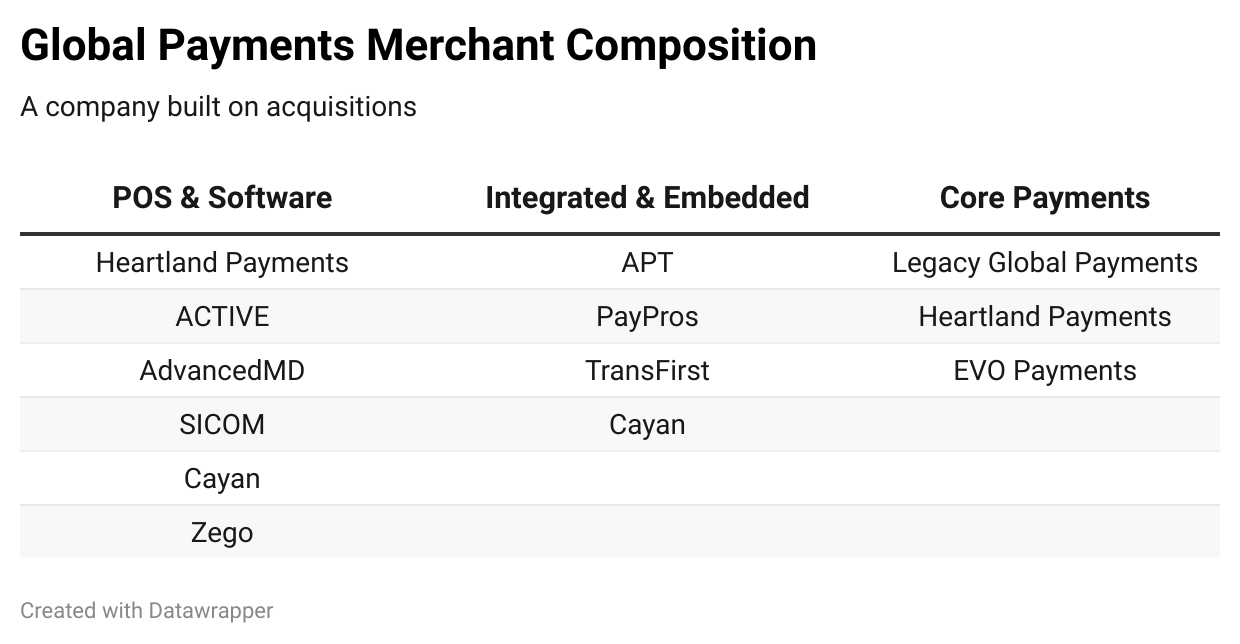

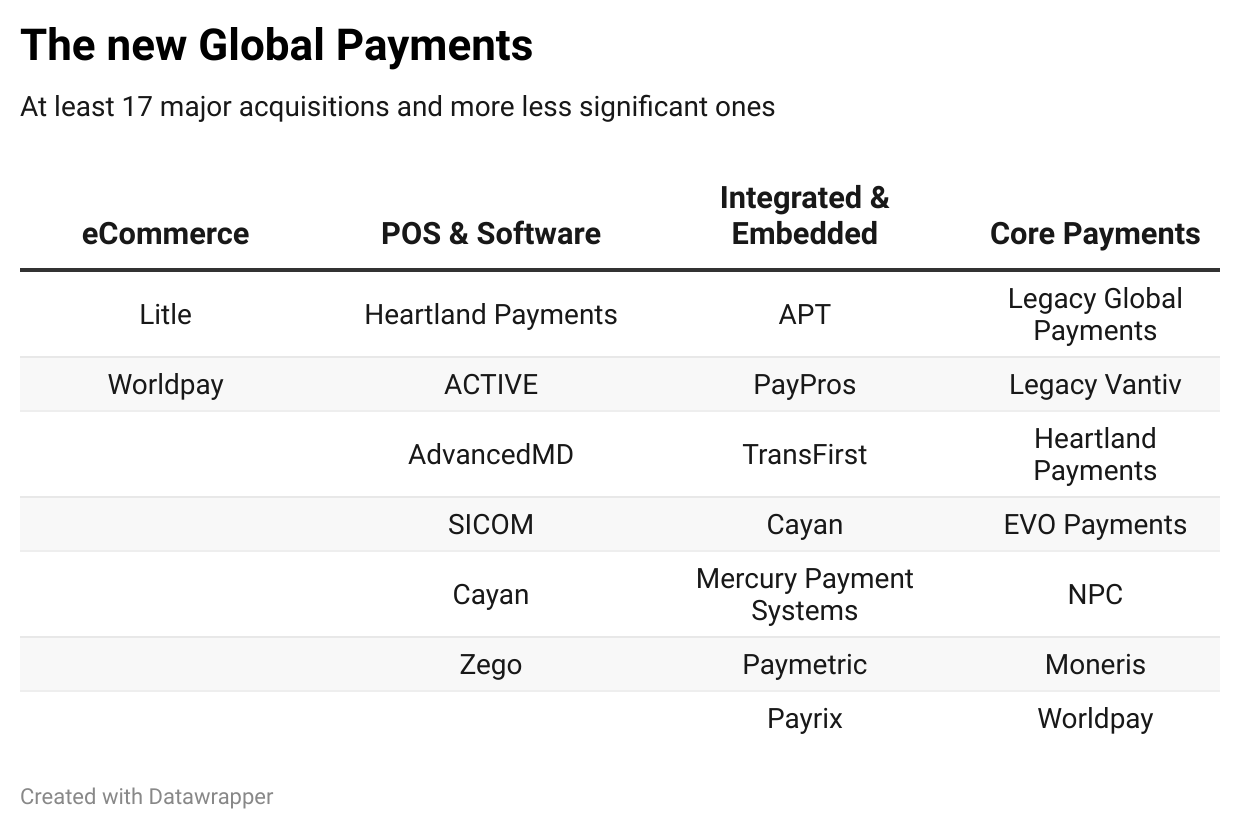

The new Global represents the combination of at least 17 major acquisitions completed since 2010, and more less significant ones

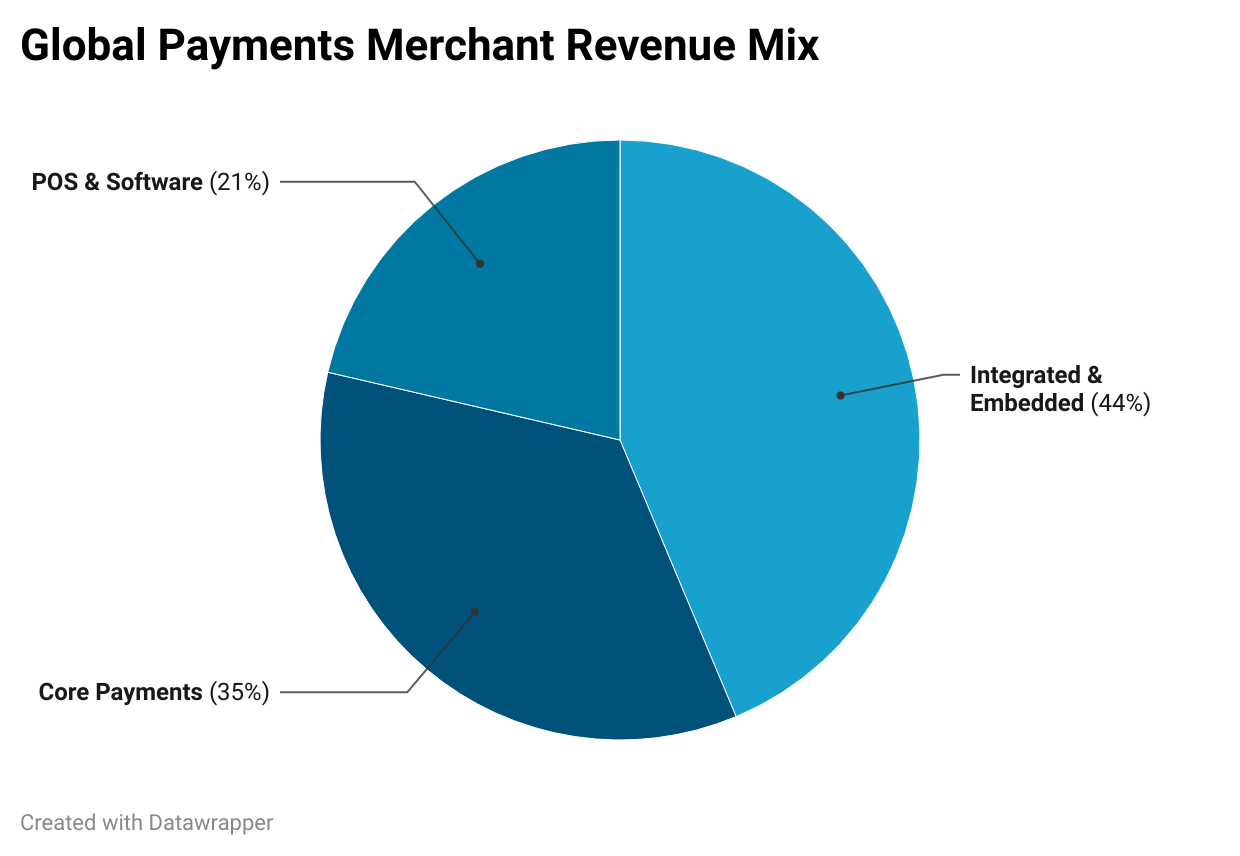

Approximately 27% of the new Global’s revenue will come from point-of-sale, software and e-commerce, the most attractive areas of payments

Organic growth up to low double-digits (LDD)

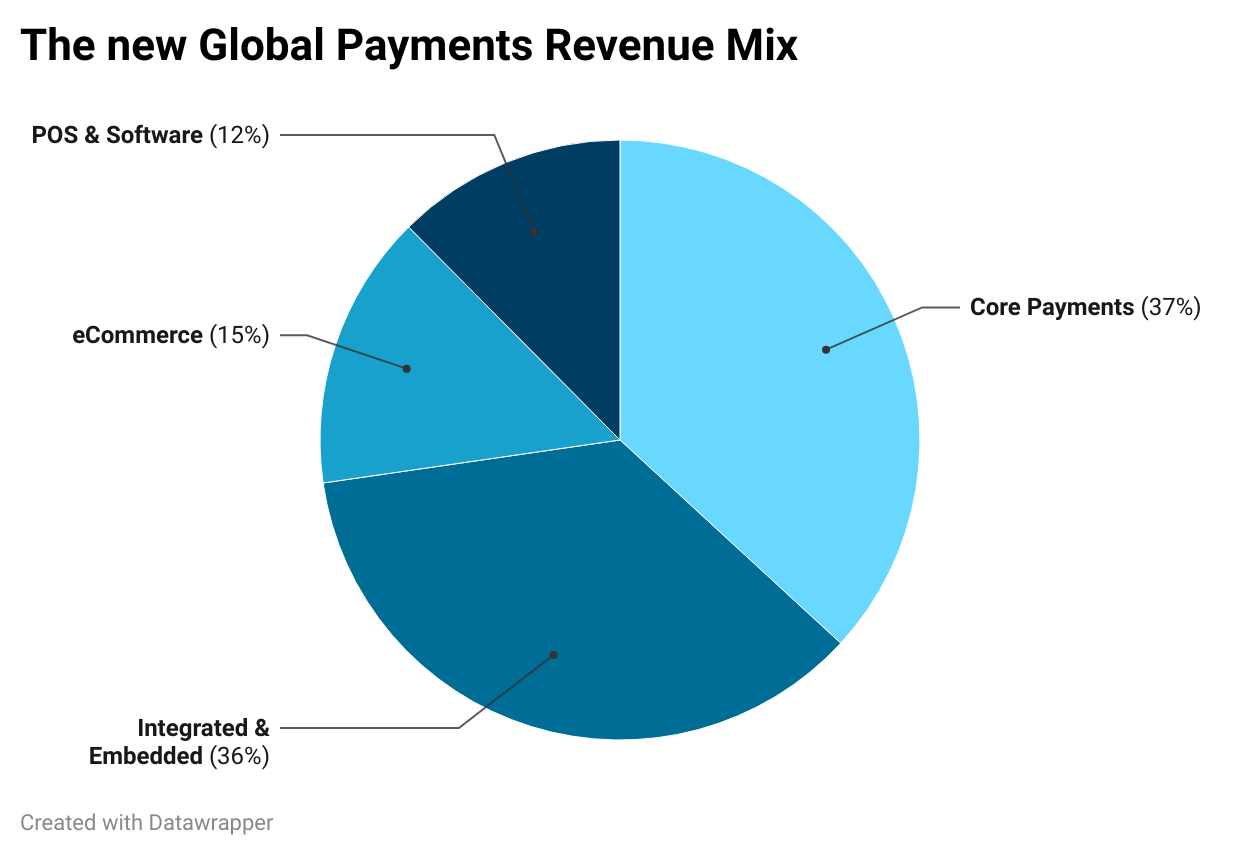

Integrated payments will represent 36% of revenue

An ongoing debate over the durability of this model as software companies move further into payments

Core payments will represent 37% of revenue

The most exposed area, but also an opportunity for the new Global to move existing merchants onto technology-enabled solutions

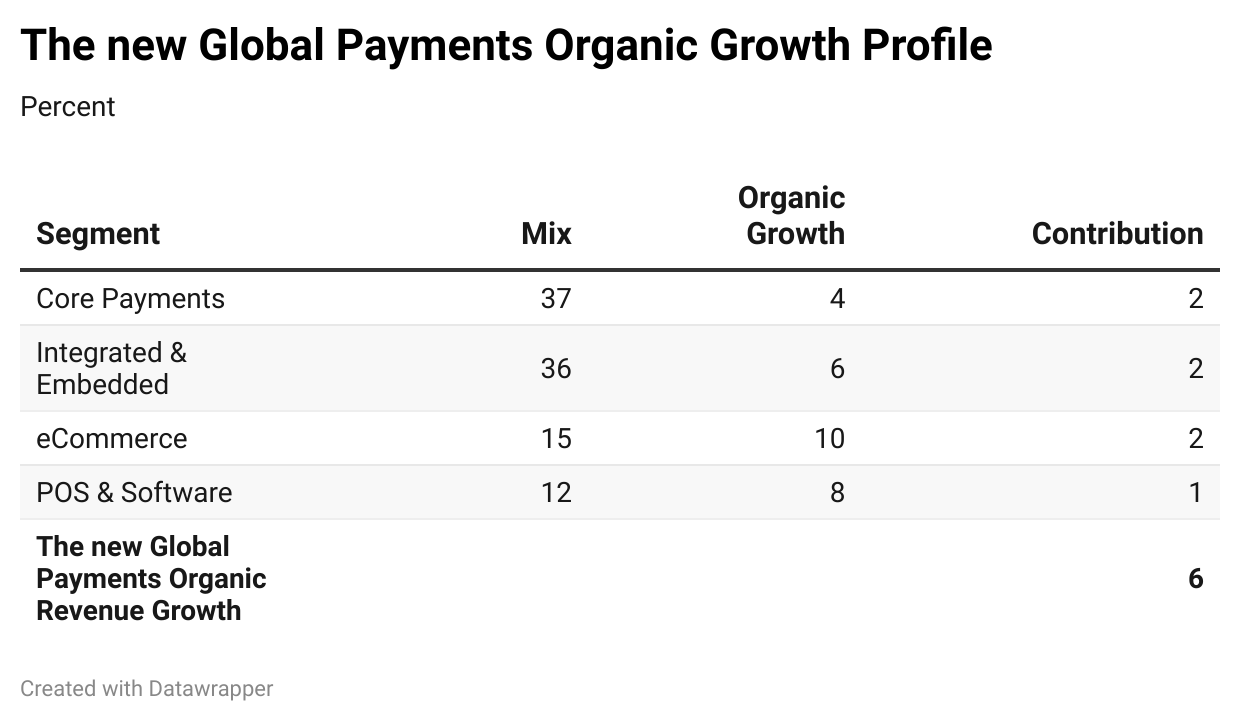

A conservatively calculated organic growth profile for the new Global of approximately 6%

Global Payments and Worldpay: Past and Present

Global Payments: Past

In the 2000s, Global found success partnering with independent sales organizations, or ISOs, to deliver basic processing solutions to small businesses. The company grew alongside its ISO partners. But the stock faltered as some ISOs became too large, gaining bargaining power over Global.

At the same time, point-of-sale software for small businesses was becoming more common. And companies had a novel idea: integrate payment processing into software.

Sensing the shift, Global pivoted. Beginning in 2012, the company acquired multiple companies1 specializing in the newly termed integrated payments.

With the acquisition of Heartland Payments in 2016, Global took the next logical step, becoming the owner of software for restaurants, schools, and universities. Additional acquisitions of software2 followed.

The acquisition of TSYS in 2019 moved the company farther afield. In addition to a merchant acquiring business, which focused on integrated payments3, TSYS brought with it a market leading issuer processing business and NetSpend, a prepaid card program manager.

Global’s last major acquisition came in 2023, with the purchase of EVO Payments, which primarily provides processing solutions to merchants in the Americas and Europe through partnership with financial institutions.

Since then, Global has taken steps to unwind past acquisitions. The company sold NetSpend in 2023 and AdvancedMD at the end of last year. The proposed swap with FIS will see Global part ways with TSYS’ issuer processing business.

Global Payments: Present

Global separates its Merchant segment into three channels:

POS & Software represents the company’s owned software and point-of-sale systems. Revenue sources are processing fees, subscription fees, and fees for other value-added services.

Integrated & Embedded represents Global’s partnerships with independent software and other platform companies. Revenue sources are processing fees and fees for other value-added services.

Core Payments represents merchants acquired through direct sales, financial institutions, and ISOs. Revenue sources are processing fees and fees for other value-added services.

In 2024, the Merchant segment of Global generated $7.1 billion of revenue. After factoring in recently competed divestitures, pro-forma 2024 revenue was $6.8 billion. The company expects organic revenue growth of 6% during 2025, offset by about a 2% currency headwind. Implying 2025 revenue of $7.1 billion.

At its 2024 Investor Day, Global laid out the following medium-term organic growth targets for its Merchant channels:

POS & Software: high-single (HSD) to low double-digits (LDD)

Integrated & Embedded: HSD to LDD

Core Payments: mid-single digits (MSD)

Adding it all up, implies organic revenue growth of approximately 7% for Global’s Merchant segment over the medium-term. Global is guiding for 6% growth in 2025. The slightly lower target accounts for disruption from Global’s effort to unify its operating structure and consolidated its retail and restaurant point-of-sale systems behind its Genius platform.

Worldpay: Past

The genesis of Worldpay was the payment processing unit of Fifth Third Bank. Fifth Third Processing, as it was called, served primarily enterprise merchants in the U.S., with significant market share of grocery stores.

During the great recession, Fifth Third sold 51% of Fifth Third Processing to Advent International, in order to boost its capital levels.

To diversify away from large merchants, Fifth Third Processing acquired NPC, a provider of processing solutions to small businesses, during 2010.

In 2012, Fifth Third Processing, now called Vantiv, entered the public markets through an initial public offering.

Sensing a similar shift as Global, in 2014, Vantiv acquired Mercury Payment Systems, a leader in integrated payments.

From 2012 through 2017, Vantiv made additional acquisitions4 that diversified the company away from enterprise merchants.

In early 2018, Vantiv closed the acquisition of Worldpay, a leader in global ecommerce, the largest merchant acquirer in the U.K., and a top 10 acquirer in the U.S. As part of the acquisition, Vantiv adopted the name Worldpay.

In 2019, FIS acquired Worldpay. And although Worldpay performed satisfactorily through part of 2022, performance deteriorated toward the end of the year. Organic revenue growth was in the low single-digits during the fourth quarter of 2022 and first half of 2023. In February 2023, FIS announced a planned spin-off Worldpay. However, later in the year, FIS decided to sell a majority stake in Worldpay to GTCR, a private equity firm, at a valuation of $18.5 billion, less than half the $43 billion FIS paid for it.

Worldpay: Present

I separate Worldpay’s business into four categories: eCommerce, Enterprise, SMB, and Integrated Payments. In each, revenue sources are processing fees and fees for other value-added services.

For 2024, I estimate Worldpay revenue of approximately $5.1 billion. The company last reported annual revenue for 2022, $4.8 billion, implying a 3% compound annual growth rate from 2022 through 2024.

During the first half of 2023, Worldpay’s organic revenue growth was approximately 2%. I assume 2% organic revenue growth for full year 2023 with:

double-digit (DD) to low-teens growth for eCommerce and

a 3% decline for the rest of the business

For 2024, based on commentary from Global, I assume 5% organic revenue growth for Worldpay with:

DD to low-teens growth for eCommerce and

a 1% increase for the rest of the business

Based on DD to low-teens growth for eCommerce during 2023 and 2024, I estimate eCommerce now makes up 35% of Worldpay’s revenue, up from 30% during 2022

According to Global’s presentation, Enterprise and eCommerce represented approximately 50% of Worldpay’s revenue. Given the 35% share for eCommerce, this implies a 15% share for Enterprise

In the same presentation, Global stated Integrated Payments and SMB each represented approximately 25% of Worldpay’s revenue

I am separating the new Global into four categories:

eCommerce: The eCommerce segment of Worldpay

POS & Software: The POS & Software segment of Global

Integrated & Embedded: The Integrated & Embedded segment of Global plus the Integrated Payments segment of Worldpay and

Core Payments: The Core Payments segment of Global plus the SMB and Enterprise segments of Worldpay

I believe an appropriately conservative organic growth profile for the new Global is 6%, based on:

4% growth in Core Payments

approximates nominal GDP growth in its largest markets of the U.S. and U.K.

6% growth in Integrated & Embedded

below HSD to low DD target for Global’s Integrated & Embedded segment

contemplates risk of software companies moving further into payments, disrupting integrated payments model

10% growth in eCommerce

below recent growth, but at-or-above global e-commerce sales growth

8% growth in POS & Software

at low-end of HSD to low DD target

assumes faster growth than integrated and core payments

Global acquired Accelerated Payment Technologies, or APT, in 2012 and Payment Processing, or PayPros, in 2014. Both acquisitions were for more than $400 million

Global acquired ACTIVE in 2017 for $1.2 billion, AdvancedMD in 2018 for $700 million, SICOM in 2018 for $400 million, and Zego in 2021 for more than $900 million

TSYS acquired TransFirst in 2016 for $2.4 billion and Cayan in 2018 for more than $1 billion

Vantiv acquired Litle (e-commerce) in 2012 for about $400 million, Moneris (SMB) in 2016 for $425 million, and Paymetric (integrated payments) in 2017 for more than $500 million