Adyen: Much ado about nothing...or something?

I view post-earnings sell-off more as opportunity than sign of weakening fundamentals

The Big Picture

Shares of Adyen are off 21% since reporting Q4 and H2 2025 results on February 12th. While the quarter and guide weren’t perfect, I don’t believe they justify this magnitude of sell-off. But alas, this is payments, and Adyen’s multiple was—and still is—on the high side, making the reaction not shocking. For this update, I plan to review Q4 and H2 2025 results and 2026 guidance, identify and discuss investor concerns, some of which I share and others I don’t, and conclude with why I view the sell-off as a buying opportunity, not a sign of weakening fundamentals. In that spirit, I’ve added to my Adyen position, upping it to 35 shares.

Results and Guidance

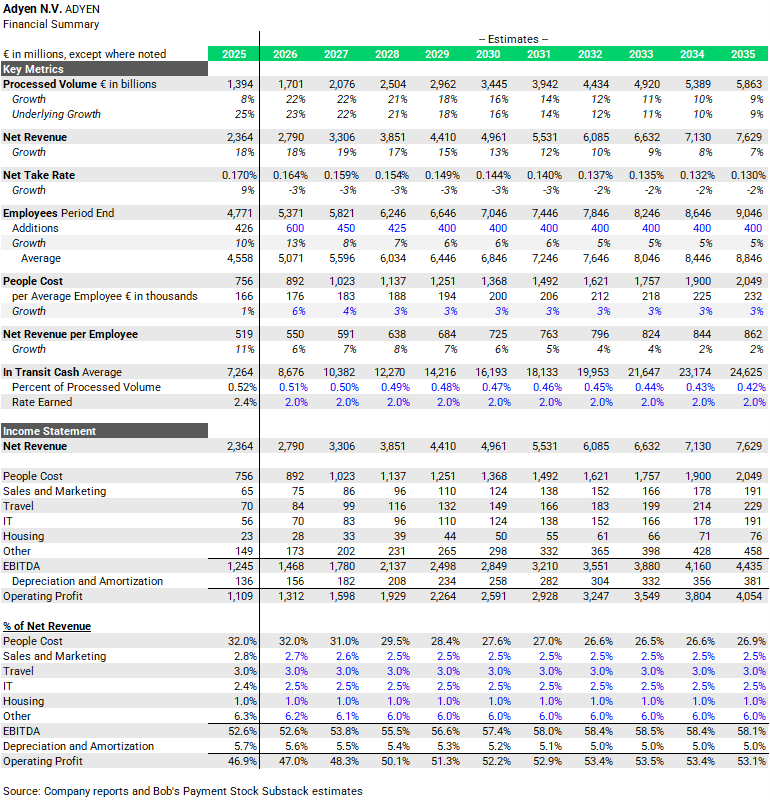

Q4 net revenue of €672 million increased 19% on a constant currency basis, down 4-points from Q3 [Adyen attributed the slowdown in Q4 to settlement timing and a difficult prior year comparison, a common refrain across payments]

H2 2025 constant currency net revenue grew 21%, similar to H1, in-line with Adyen’s lowered guidance [Following its H1 2025 update, Adyen lowered its expectation for 2025 constant currency net revenue growth to being broadly in-line with H1 (+21%), down from its previous guidance for a slight acceleration in 2025 versus 2024 (+23%), due primarily to lower market volume growth]

The strengthening of the euro against a basket of major currencies created a larger headwind for Adyen in Q4, reducing constant currency revenue growth by 4-points, resulting in reported net revenue growth of 15%

Processed volume grew 15% in Q4 [After excluding the impact of Cash App and foreign currency, I estimate underlying processed volume grew 23% in Q4, similar to the first three quarters of 2025, notable given the difficult comparison from Q4 2024]

H2 2025 EBITDA1 of €702 million increased 25%, with margin of 55% expanding 340-bps versus prior year

2025 EBITDA of €1,245 million, with a margin of 53%, up 320-bps

Adyen ended 2025 with available cash2 of €4,426 million and no debt

Free cash flow, which I define as cash generated from operations adjusted for the impact of settlements (netting receivables from and payables to merchants and financial institutions), was €1,120 million in 2025, representing 105% of Adyen’s net profit

Adyen’s top 10 merchant customers represented 11% of revenue in 2025, down from 12% in 2024, and 53% in 2017

Adyen expects 2026 constant currency net revenue growth of 20-22% [With Q3 2025 results, and reiterated at its capital markets day in November, Adyen guided 2026 constant currency net revenue growth of ‘low-to-mid 20%’]

Adyen expects 2026 EBITDA margin to be ‘broadly in-line’ with 2025 [Adyen did not previously provide specific 2026 EBITDA margin guidance, only an expectation that EBITDA margin would exceed 50% in 2026 and 55% by 2028]

Investor Concerns

Revenue guidance ‘cut’. Over the span of six months, Adyen’s 2026 constant currency net revenue growth outlook fell from ‘low-to-high 20%’ to ‘low-to-mid 20%’ to 20-22%. While the original ‘low-to-high 20%’ range was provided as part of a multi-year outlook, which was ending in 2026, the ‘low-to-mid 20’ range was tailored specifically for 2026, provided as part of the Q3 business update and reiterated at Adyen’s capital markets day in November. Although Adyen prefers to frame the most recent 2026 constant currency net revenue forecast as a refinement based on in-depth customer planning and conversations, the market is taking a decidedly more skeptical view. Optically, the move down to the lower end of the range is never pleasing, especially so soon. However, the reality of the situation is that Adyen’s constant currency net revenue growth for the four years through 2026 is expected to be: 22%, 23%, 21%, and 21%, assuming Adyen lands at the midpoint of its 2026 forecast. I do not view this trend as overly concerning, but a natural moderation in growth as Adyen becomes larger, and one I expected. In fact, an optimist (are there any of those left in payments?) would argue Adyen’s ability to sustain attractive growth as it scales should be celebrated, not denigrated.

Of course, the bears will counter Adyen’s recent guidance track record is decidedly mixed, calling into question the veracity of its 2026 forecast. And they have a point, a strong case in fact. At its 2023 capital markets day, Adyen laid out a constant currency net revenue growth target of ‘low-to-high 20%’ for 2024, 2025, and 2026, and then proceeded to do 23%, 21%, and 21%. Not exactly hitting the lights out. For 2025, Adyen believed constant currency net revenue growth would accelerate ‘slightly’ versus 2024, which was up 23%, suggesting 24% growth, at minimum. They did 21%. Thud. The reality is that while absolute trends are not concerning, Adyen needs improvement properly setting expectations. Until the markets are comfortable that has been done, upside may be capped.

Flat EBITDA margins in 2026 with a reacceleration in headcount growth. To me, this is the most interesting, and potentially concerning development for Adyen. While peers are dialing back headcount, or even slashing it in the case of Block, Adyen plans to hire 550-650 net new employees in 2026, representing 12.5% growth at the midpoint, on top of 10% growth in 2025. While Adyen frames it as investing to capture long-term growth opportunities, the market sees other companies sustaining attractive top line growth with stable-to-declining headcount and asks why Adyen can’t do the same? It’s a fair question and one I don’t have a good answer for. Is it a cultural issue? Maybe pride? Although I’m sure Adyen’s management would like to see the stock price move higher, they’re certainly not moved enough by the declines to change the path they’re on, and their belief that Adyen is still at the early days of its growth potential. In their defense, Adyen is already a highly profitable business, and the company has seen significant expansion in its EBITDA margin since it bottomed in 2023, following Adyen’s significant hiring during 2022 and 2023. Plus, Adyen still expects its EBITDA margin to move above 55% by 2028, suggesting a resumption of gains in 2027 and 2028. However, when it comes to the numbers, Adyen’s performance and standing do not paint a pretty picture:

Among payments and fintech peers, Adyen’s employment growth has been the most significant since 2019—up 4.5x through 2026—and while some companies are still growing headcount, many are not

Adyen’s net revenue per average employee of $588k in 2025 is at the very low end of payments and fintech peers and level with 20193

All of this contributes to no meaningful change in Adyen’s 2026 EBITDA margin versus 2018 and a 10-point drop from its high water mark in 2021

My gut feeling is that Adyen will find ‘religion’ on headcount growth at some point. While that time is not now, I think the market will eventually force its hand if it does not arrive at the decision voluntarily. At that point, I believe inflection in profitability will be more significant.

Lack of capital return or allocation ‘policy’. I really don’t view this criticism as fair. I believe Adyen’s fortress-like balance sheet is a source of strength, giving them significant flexibility to pursue both organic and inorganic opportunities—when the time is right. While it’s natural for investors to want companies to return excess capital when it builds on the balance sheet, I applaud Adyen for not rushing out to buy its own stock when it was excessively high. Of course, with valuations more attractive now, a share buyback would make sense, but I’m not going to punish Adyen for abstaining. Adyen’s priority remains retaining capital on its balance sheet in support of its financial products roadmap, which includes card issuing, accounts, and lending, key attractions for platforms and the small business customers they serve. I, for one, believe this is an excellent use of capital.

Behind in agentic commerce? I tend to side strongly with—or at the least not punish—Adyen’s measured approach to agentic commerce, which has involved more than 100 in-depth customer interviews to gauge their ‘hopes and fears’ regarding the nascent technology. To be clear, agentic commerce today is not measurable. Can it become something much larger over time? Of course. Is that guaranteed to happen? No. What’s happening now is largely theatrics. Dueling press releases. Collaborations teased. Protocols being written. Adyen is responsibly taking action to prepare itself, and its customers, for agentic commerce. But don’t mistake Adyen’s lack of chest thumping as indifference to the threats or opportunities posed by agentic commerce. Ultimately, Adyen’s structural advantages in a world of human commerce is likely to translate to a world of AI agents: a single technology platform with an end-to-end view of transactions in real-time, allowing Adyen to dynamically identify and validate AI agents, boosting conversion, lowering fraud, and building trust in a new system.

My Thoughts on the Stock

From my perspective, very little has changed for Adyen, except a lower share price, which is a good thing! My view of the company’s growth profile, although somewhat below the market’s, is unchanged. While I was hoping for more significant margin expansion over the near-term, I believe Adyen is still capable of reaching a 60% EBITDA margin over the medium-term. The end result is that my fair value for the company is little changed. Here are my key assumptions, and how they’ve changed since my last update:

For 2026, I assume reported net revenue growth of 18%, which is down from my prior forecast of 20%, primarily reflecting a larger FX headwind. My 2026 net revenue estimate assumes 20% constant currency growth, at the low-end of Adyen’s guidance, with 2-points of FX headwind, larger in H1, and moderating in H2. On the expense side, I assume Adyen hires 600 net new employees ratably over the year and cost per employee rises by 6%, as Adyen hires disproportionately in more expensive markets, like the U.S., and for specialized skills. The end result is that people costs4 equal 32% of net revenue in 2026, similar to 2025, following a 310-bps decline from 2024 to 2025. With those changes, my EBITDA estimate falls to €1,468 million, down from my previous €1,548 million estimate. The 2026 EBITDA margin of 52.6% is dead even with 2025 and about 150-bps below my prior estimate.

Beyond 2026, I continue to expect moderation in constant currency net revenue growth, falling to 10% by 2032 and 7% by 2035. Even though I still believe Adyen can—and will—reach an EBITDA margin of 60%, or more, for the sake of conservatism, I now assume a maximum EBITDA margin of 58.5% in 2033, about 2-points below my prior forecast, as people costs fall to only 26.5% of net revenue by 2033, 150-bps above 2018. My forecast for in-transit cash balances and average yield (about 2%) remain largely unchanged versus my prior forecast.

Holding all else equal in my DCF model, specifically the discount rate and terminal growth rate, my new fair value for Adyen is €1,435 per share, about a 4% reduction from my prior €1,499 estimate, and still representing nearly 60% upside from current prices. If I raise my discount rate to 10%, from 9%, and lower my terminal growth rate to 3.5%, from 4%, my fair value estimate declines to about €1,150, still representing more than 25% upside.

As always, thank you for reading, and if you’ve enjoyed this, please consider sharing, liking, commenting or subscribing!

Disclosure: As of March 17, 2026, of the stocks mentioned in this report, I am long Adyen and Block. This report is for informational purposes only and is not a recommendation to buy or sell any stock. Finally, while I rely on the information in this report to guide my investment decisions, you should not, because I cannot guarantee its accuracy.

Unlike Adyen, I exclude other income from my EBITDA calculation. In 2025 and 2024, other income was €1 million and €7 million, respectively

Available cash equals cash and cash equivalents (€10,797 million) minus payables to merchants and financial institutions (€6,372 million)

Adyen generated €520k and €519k of net revenue per average employee in 2019 and 2025, respectively

People costs represent wages and salaries plus social securities and pensions costs

Thank you!

From what I know about Adyen they are running a tight ship in terms of operations and most recent hires are for banking

Think you are conservative on outer yrs revs, platforms can be 5-10% of revs in few yrs

Though didnt like the guidance dance at all… not sure what was the issue between Nov to Feb… odd