Payroll and HCM Primer

Intuit, ADP, Workday, Paychex, Paycom Software, and Paylocity

One of my goals this year is to expand coverage. First up is payroll and HCM1. Unlike payments and FinTech, I thought I would flip the script, leading off with a broad overview of the sector, then follow-up with detailed company reports.

Investment Brief

Payroll and HCM companies, including even mature ones like Automatic Data Processing (ADP) and Paychex (PAYX), have enjoyed premium valuations for most of the past decade, largely due to their mission-critical solutions (no business can skip payroll, or risk it being wrong), sizable TAMs, pricing power, strong balance sheets, and rational capital allocation. However, those premiums are disappearing as some cyclical tailwinds fade, and AI’s emergence creates both risks and opportunities:

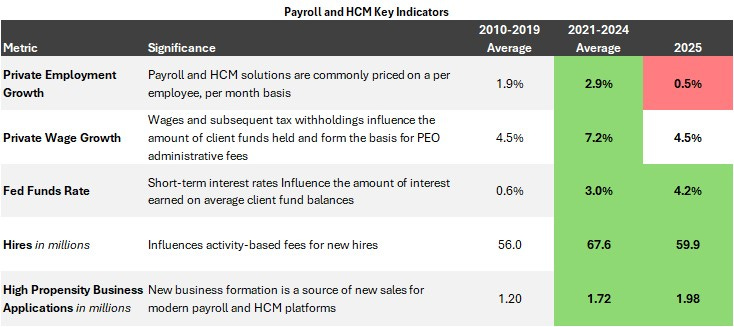

In the years following the pandemic, the payroll and HCM industry benefitted from an almost perfect environment: a strong recovery in employment, rapidly rising wages and short-term interest rates, significant labor market turnover, robust new business formation, and exceptional demand for HCM solutions by small businesses looking to attract talented employees in a highly competitive labor market, all backed by extraordinary government support, including the employee retention tax credit, or ERTC, which netted small businesses hundreds of billions of dollars through 2025.

Now, some of those tailwinds are fading. Employment growth has slowed to a standstill, and short-term interest rates are falling. Still, even though other parts of the labor market and economy are moderating, they remain at-or-above pre-pandemic levels, including wage growth and new business formation, which was especially strong during 2025:

Like other software companies, payroll and HCM providers have not been immune to speculation about AI’s impact on their businesses. While all payroll and HCM companies have touted efforts to incorporate AI into internal operations, service models, and customer-facing products, investors increasingly question whether the system-of-record model remains viable in a world where AI can easily ingest, analyze, and act on large amounts of data at little cost. Believe me, the purpose of this article is not to definitively declare whether AI will kill software. I don’t know the answer to that question. Instead, I will provide my thoughts on how I believe AI may impact the payroll and HCM industry:

Regulatory complexity does not protect incumbent payroll providers from disruption. Although tax and employment laws across multiple states and countries create significant complexity for employers, which modern payroll and HR systems address with accrued human expertise, these laws, rulings, and guidance exist in the public domain. Therefore, AI should be assumed capable of developing and maintaining an accurate and reliable system to rival, not surpass, current ones.

Payroll and HCM providers serving small businesses are more protected. While it’s reasonable to believe that some, or most, large businesses will try to displace third-party vendors with internally developed software aided by AI, it seems unrealistic that many small businesses would have the resources required to replicate and maintain modern payroll and HCM systems. Still, AI is likely to spur significant competition and create viable, and possibly cheaper, alternatives. Although that poses a risk, incumbents benefit from existing customer relationships, trusted brands, large sales forces, proprietary data, and their own AI efforts.

Proprietary data holds value. Even though tax and employment laws are in the public domain, incumbent payroll and HCM providers have access to significant proprietary information, including existing customer data and all interactions employees and HR professionals have with their systems over time. This may allow incumbents to stay ahead of prospective challengers by developing and delivering a more intelligent platform for customers.

The potential for a secular decline in employment. In addition to the impacts AI will have on the creation and performance of software, it also has the potential to affect employment as AI agents displace human workers, especially white collar or knowledge-based ones. While fewer employees equaled less revenue under the old model, it is not clear how agents will be monetized in a new world of AI, including those deployed by payroll and HCM companies, as well as employer-based agents that interact with payroll and HCM systems.

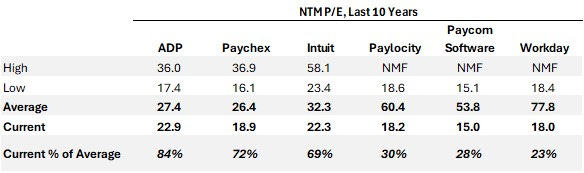

My thoughts on the stocks. Even though headline multiples have declined to a reasonable level, all stocks are not compelling…yet, especially considering alternative measures of valuation, such as price-to-free cash flow excluding stock-based compensation:

My order of preference is Intuit, ADP and Paychex:

Intuit (INTU) has phenomenal franchises in TurboTax and QuickBooks, which dominate their respective categories and are less prone to AI disruption given their consumer and small business focus.

ADP is the most well rounded HCM player but still has significant small business exposure. Additionally, their unique client funds investment strategy may result in an improvement in realized yield over the next couple of years even as short-term interest rates fall.

Paychex is an elite dividend stock, yielding close to 4% with dividend growth up to the high single-digits. Their small business focus is a plus, but the Paycor HCM acquisition has not gone exactly according to plan.

I’m less enthused about Workday (WDAY), Paycom Software (PAYC) and Paylocity (PCTY) given their valuations and exposure to enterprise customers (Workday) which are more susceptible to AI disruption, and the middle market (Paycom and Paylocity) where competition is heating up.

Payroll and HCM Market

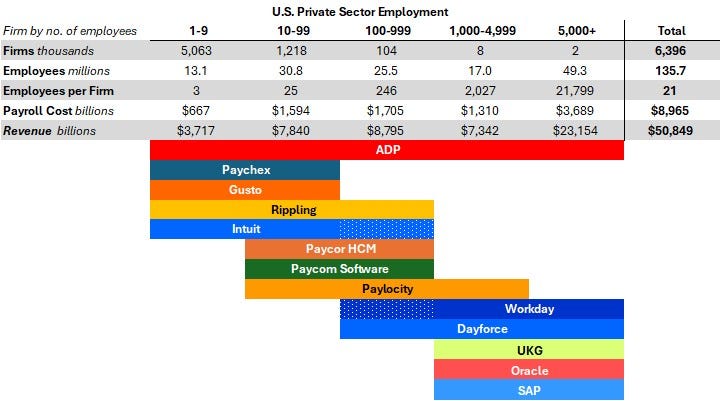

As of 2022, the last time detailed information was shared, there were approximately 6.4 million private sector businesses in the U.S. employing 135.7 million people:

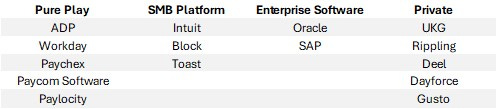

In addition to the option of manual preparation and small regional providers, the major players in payroll and HCM are:

Below is my estimate of U.S. payroll market share:

And where each company plays in terms of client size:

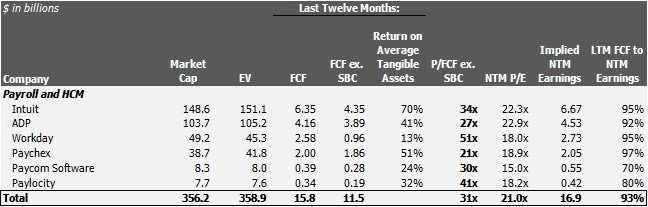

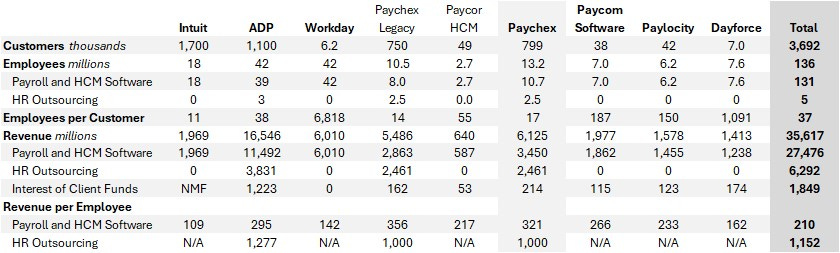

Across the industry, payroll and HCM software generates $210 of revenue per employee per year. A couple of observations (from the table below):

Enterprise-focused companies (Workday and Dayforce) generate less payroll and HCM software revenue per employee. I believe there’s two reasons for this. First, as in all business, enterprise customers with higher volume typically generate lower per unit revenue. Second, Workday and Dayforce do not provide payroll to all their customers, unlike those companies focused on small businesses and the middle market. As a matter of fact, only 63% of Workday’s HCM customers attach payroll while up to 90% of customers attach payroll with Dayforce.

Small business-focused companies likely generate more payroll and HCM software revenue per employee, as is the case with Paychex’s legacy business ($356 per employee per year). Once again, small businesses with less volume typically generate higher per unit revenue. Second, all small business customers are payroll customers. And, finally, in the case of Paychex’s legacy business and ADP’s small business segment, the attachment of additional products, including retirement, boosts revenue per employee.

Intuit generates the least amount of payroll and HCM software revenue per employee, even though they are focused almost exclusively on small businesses, likely because they provide only payroll (and not other HCM solutions), with more customers than not selecting a basic solution.

A full HR outsourcing solution generates substantially more revenue per employee ($1,152) than payroll and HCM software ($210).

I estimate a U.S. payroll and HCM software TAM of $72 billion. This not too scientific estimate is informed primarily by individual company estimates, arrived at by multiplying the number of employees in a category by revenue potential from adoption of a full product suite. As the table below demonstrates, I assume a decline in per employee, per month pricing as client size increases. Overall, my estimate implies about $530 in annual payroll and HCM software revenue per employee, suggesting about 40% penetration based on the current $210.

Payroll and HCM Solutions and Revenue Models

The payroll and HCM industry generates revenue from four primary sources: (1) fees for payroll and HCM software; (2) fees for full HR outsourcing; (3) implementation and professional service fees; and (4) interest earned on funds held for clients.

Payroll and HCM Software. Payroll and HCM companies offer cloud-based software platforms that include payroll processing and other HCM solutions covering the entire employee lifecycle, from ‘hire to retire’. While revenue models vary, the most common is per employee, per month, or PEPM, pricing, with revenue determined by the number of employees and solutions (or modules) adopted. Smaller businesses may pay a fixed monthly fee plus a fee per employee. Other models are activity-based, including a flat fee per payroll run, a fee per employee paid, or a fee for each new hire. Below is an overview of the most common payroll and HCM software solutions:

Payroll. Wages, taxes and withholdings are calculated based on information provided by the employee and applicable state and local laws. Funds are collected from the employer and paid to employees electronically, via paper check, or to a prepaid card. Reports are prepared for accounting reconciliation. Taxes are collected, held and remitted to the proper agencies.

HR Information System. A centralized dashboard where employees can access corporate policies and provide personal information, including home address, marital status and number of dependents.

Time. Tracks attendance and time worked. Provides tools and analytics for scheduling shifts and requesting time off or leaves of absence.

Talent. Handles the hiring process, from creating a job description, posting on popular job forums, screening applicants, managing the interview process, determining appropriate compensation, and onboarding new employees.

Engagement. Spans a wide range of programs, including employee wellness, learning and performance tracking.

Benefits. Manages the procurement, selection and administration of benefits, including medical, spending and retirement plans offered by payroll and HCM companies or third parties.

Full HR Outsourcing. Select payroll and HCM companies offer a full human resource outsourcing solution to employers, spanning payroll, compliance, time and talent, benefits administration and insurance. Under the professional employer organization, or PEO, model, the PEO becomes the co-employer of record completing eliminating employee-related liabilities for the employer. In return for this peace of mind, employers pay significantly more per employee for a full outsourcing relationship. An administrative fee based on a percentage of employee wages can be several times higher than per employee, per month pricing for payroll and HCM software. As an example, I estimate ADP generates up to $3,200 per employee under its PEO model compared to less than $300 per employee for its payroll and HCM software.

Implementation and Professional Services. Some payroll and HCM companies charge a one-time fee to customers for the implementation of its platform and to onboard employees and transfer data.

Interest on Client Funds. Payroll and HCM companies hold client funds earmarked for payroll (for a very short period) and tax payments (typically held for up to a month but can be up to 90 days) creating float, which the companies invest in highly liquid and secure short-term debt instruments, generating interest income, which they count as revenue. The size of client fund balances depends on a couple factors, including wages, withholding requirements, and withholding timelines.

Payroll and HCM Key Themes

Pricing power at the low end of the market. Unlike payments, where providers serving small businesses maintain pricing but cannot raise it, payroll and HCM companies in the small business market have historically been able to increase prices. Paychex, whose average customer has 14 employees, has long discussed implementing annual price increases in the 2-4% range. While not providing specifics, Intuit (11 employees per customer) frequently cites ‘higher effective pricing’ and ‘mix-shift’ as contributors to payroll revenue growth. Finally, ADP, which serves clients of all sizes, achieves annual price increases of 0.5-1.5%, with hikes likely largest among its small business customers.

AI initiatives. Payroll and HCM companies are rolling out AI assistants (i.e., chatbots) and incorporating the technology into internal functions, such as sales. Select highlights include:

The Zone is an AI-powered tool for ADP’s sales force, promising to put them in front of the right buyer, at the right time, with the right product, and message. ADP Assist is an AI-powered assistant embedded across ADP’s products—over the last year, more than 5.5 million clients have conversed with ADP Assist.

IWant by Paycom allows users to access employee information and HR data from its single database through either a voice or typed command.

Intuit recently launched the Intuit Payroll Agent for mid-market businesses that automates the collection of accurate payroll information.

Usage of Paylocity’s AI-powered features have more than doubled over the past year and include more than 1.2 million questions answered by the company’s AI assistant.

Middle market focus. The middle market is becoming increasingly crowded as Intuit moves upmarket, Workday moves down, and Paycom and Paylocity drift upward to larger client sizes. In late 2024, Intuit launched Intuit Enterprise Suite, a single platform incorporating the full breadth of Intuit’s solutions, targeting businesses with $25 million or more in revenue. With the inclusion of GoCo, a recently acquired provider of HR and benefits solutions, Intuit is going to market with a more comprehensive payroll and HCM platform. Likewise, in mid-2025, Workday announced Workday GO, a combined HR and finance platform designed specifically for small and mid-sized businesses.

Step-up in M&A. For an industry that historically sees limited acquisition activity, the last 18 months have been more eventful, highlighted by:

Paychex’s acquisition of Paycor HCM for more than $4 billion

Thoma Bravo’s $12 billion deal to take Dayforce private

Workday’s acquisitions totaling about $3 billion since 2024, focused primarily on integrating AI capabilities into its platform

ADP’s $1.2 billion deal to buy WorkForce Software, a provider of workforce management software for enterprise customers

Paylocity’s $325 million deal to buy Airbase, a provider of spend management software

I do not believe it is outside the realm of possibility that Intuit or Workday would acquire either Paycom or Paylocity to boost their middle market presence, given that market’s strategic importance to both companies. However, given their organic efforts to date, an acquisition today seems less likely.

Still, given Paycom’s and Paylocity’s size (less than $10 billion market cap) and financial profile (significant recurring revenue and net cash position), a takeout by private equity should not be dismissed.

Embedded payroll. Much like embedded finance or integrated payments, embedded payroll involves integrating payroll processing directly into third-party business management software. The best example is ADP adding RUN, its payroll and HCM platform for small businesses, into Clover, Fiserv’s business management software for small businesses. While this strategy offers additional distribution opportunities for payroll providers—a positive—it also poses long-term risks if software companies decide to become more involved in payroll, as they have with payments, potentially pressuring economics for payroll providers or displacing them entirely. Notably, complete commerce platforms already exist in the market, including Intuit, Block, and Toast.

Odds and Ends

Before getting to company profiles, there are a couple key areas where payroll and HCM companies differ that I believe are important to note:

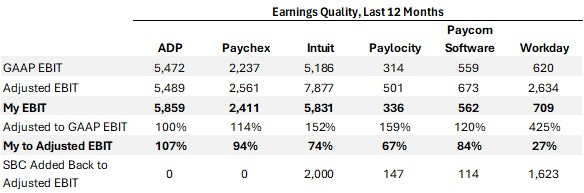

Earnings Quality. Much like payments, mature payroll and HCM companies (ADP and Paychex) have better earnings quality and make fewer adjustments to GAAP results. On the other hand, faster-growing payroll and HCM companies (Intuit, Workday, Paycom and Paylocity) have more add-backs, including significant stock-based compensation expense:

Note, My EBIT represents GAAP EBIT + the amortization of acquired intangible assets

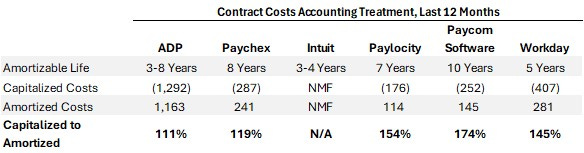

Contract Costs Accounting Treatment. All payroll and HCM companies incur costs to obtain and fulfill contracts that are capitalized upfront and amortized over time. The amortizable life differs by company:

At 10 years, Paycom has the longest amortizable life for contract costs, which has the effect of overstating GAAP results relative to peers with shorter lives. For example, of the $252 million in capitalized contract costs added over the past year, Paycom will amortize $25 million in the upcoming year. If the life were 7 years, as for Paylocity, amortization would be $36 million, 43% higher.

Client Funds Strategy. While Paycom and Paylocity invest client funds nearly exclusively in short-term instruments, including money market securities and other cash equivalents, generating yields more in-line with the federal funds rate, Paychex and ADP take different approaches with longer duration:

As of November 30, 2025, Paychex’s available for sale securities portfolio—which include ABS, corporate and municipal bonds, treasuries, and agency securities—had a duration of 3 years.

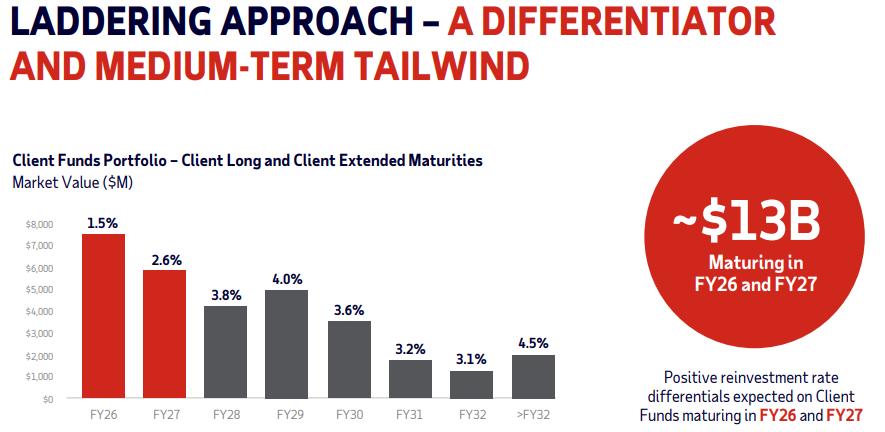

ADP invests client funds in longer-dated instruments, using short-term borrowings to meet client obligations. The practical effect of this strategy is that ADP will generate higher relative yield on its investment portfolio when short-term interest rates are low, and lower relative yield when short-term interest rates are high, as they have been for the past couple of years. Even so, with rates staying high, ADP will have the opportunity for positive reinvestment rates on $13 billion of its total $28 billion client funds extended and long portfolio over the next two years:

Company Profiles

ADP. Founded in 1949, ADP pioneered third-party payroll processing, acting as the original service bureau before developing modern platforms that rival today’s cloud-first competitors. The company later expanded into technology solutions for auto dealers and shareholder proxy delivery and processing services, businesses they eventually spun off. Today, ADP is the largest and most diverse provider of payroll and HCM solutions, serving clients from a few employees to the world’s largest businesses, including paying 16 million employees outside the U.S. In addition to payroll and HCM software, ADP offers full-service human resource outsourcing through its administrative service offering (ASO) and its professional employer organization, TotalSource, which uses a co-employment arrangement to ease the compliance burden for small businesses and secure better insurance rates and employee benefits. ADP generates more than $2.5 billion in new business bookings each year from its significant sales force and partner channels, including CPAs and banks.

Paychex. Historically serving the smallest businesses with payroll and a growing list of HR solutions, Paychex recently acquired Paycor HCM to move up to the lower end of the middle market. Paychex offers the most complete service model, ranging from do-it-yourself software (SurePayroll), assisted preparation, cloud-based HCM platforms (Paychex Flex and Paycor by Paychex), and full HR outsourcing, including through its professional employer organization, among the largest in the U.S. The company’s focus on expense discipline and operational excellence makes it the most profitable in the industry. Founder Tom Golisano, who still owns nearly 11% of Paychex, served as Chairman of the board until 2021 and a director until the middle of last year. Paychex has a generous shareholder return policy, paying out about 80% of its earnings as dividends, resulting in a current yield of nearly 4%.

Paycom Software. Led by founder Chad Richison, Paycom serves the middle market with a highly automated payroll and HCM solution delivered via software as a service (SaaS). Paycom is unique in several ways. First, the company discourages third-party integrations, positioning its offering as an all-in-one solution with a centralized database acting as a single source of truth, eliminating opportunities for errors due to duplicative data entry across third-party applications. Second, Paycom relies on advertising and a direct sales force to drive new business sales as opposed to a partner channel or referral network. Finally, Paycom operates its own data centers, resulting in higher capital intensity relative to peers that rely on cloud service providers like Amazon, Microsoft and Google.

Intuit. In addition to its popular consumer tax service, TurboTax, Intuit operates a leading small business platform anchored by its dominant accounting suite, QuickBooks, with additional offerings for payroll, payment processing, bill pay, capital, and marketing through Mailchimp. Although Intuit has focused on providing payroll as an add-on, it recently acquired GoCo, a provider of HR and benefits solutions for small and mid-sized businesses. Intuit plans to integrate GoCo with its payroll solution to deliver a modern HCM platform, including within the Intuit Enterprise Suite, an ERP-like solution for mid-market companies. According to Intuit, more than 1.7 million businesses use its payroll solution to pay 18 million employees in the U.S. annually.

Both Block’s Square and Toast incorporate payroll into their business management software. At Toast’s 2024 investor day, the company stated that 25% of customers attach its Team Management Suite, which includes payroll and scheduling. This implies about 30,000 restaurants used Toast payroll in mid-2024. Assuming 15 employees per restaurant means 450,000 employees paid (update: Toast’s website claims it processes payroll for more than half a million employees every month), and using $100 of revenue per employee—similar to Intuit—implies annual revenue of about $45 million, representing roughly 5% of the company’s subscription revenue over the trailing twelve months.

Paylocity. With its acquisition of Airbase, a provider of spend management software, and recent expansion into information technology (IT) management, Paylocity is moving beyond a traditional cloud-based payroll and HCM solution to offer a unified platform for small and mid-sized businesses across HCM, finance and IT. Although Paylocity’s platform is built on a single employee system of record, it offers integration with hundreds of third-party providers through its marketplace, including retirement plans, benefits and insurance. Since it does not offer competing solutions, Paylocity relies on third-party providers in its marketplace for referrals, including 401(k) advisors, benefits administrators and insurance brokers. In the most recent fiscal year, approximately one-quarter of Paylocity’s new business sales came from referrals.

Workday. The original cloud-first ERP system for enterprise customers—initially focused on HCM, then financial management—Workday has steadily gained share from legacy on-premise vendors like SAP and Oracle. The company is now moving down market with Workday GO for mid-sized businesses and a partnership with Insperity to offer full-service HR solutions to small businesses. At the same time, Workday is infusing AI across all aspects of its business, deploying its own agents to perform repetitive HR and finance tasks, while enabling customers to build their own agents. Workday’s stock has done absolutely nothing over the past five years, even though the company has grown the top line and successfully transitioned to GAAP profitability. Workday’s use of stock-based compensation remains egregious, representing more than 17% of revenue over the last twelve months. As a result, even though shares may look attractive on an adjusted earnings basis, on free cash flow excluding stock-based compensation, shares are still expensive.

UKG (Private). Formed in 2020 through the merger of Kronos and Ultimate Software, UKG serves primarily enterprise customers across the globe with payroll and HCM solutions. According to the company’s website, UKG has over 80,000 customers and tens of millions of users. While much of the company’s financials are unknown, UKG did report that it crossed $1 billion of revenue in the quarter ending December 31, 2022, suggesting an annual revenue run rate likely in excess of $5 billion currently.

Deel (Private). Recently valued at $17.3 billion, Deel provides a global payroll platform allowing businesses to easily expand their workforce in international markets. According to media reports, Deel recently surpassed an annual revenue run rate of $800 million.

Rippling (Private). Similar to Paylocity, Rippling offers a unified platform across payroll, HCM, finance and IT management to over 20,000 small and mid-sized businesses. The company was recently valued at $16.8 billion and reported an annual revenue run rate of $570 million as of early 2025.

Gusto (Private). Originally launched as ZenPayroll, Gusto provides a cloud-based payroll and HCM platform directly to small businesses as well as by embedding it with partners, such as JPMorgan. Recently valued at near $10 billion, Gusto is believed to have up to 400,000 customers and several hundred million dollars of annual revenue.

Dayforce (Private). Recently taken private by Thoma Bravo for $12 billion, Dayforce serves both enterprise and small business customers with payroll and HCM solutions primarily across Canada and the U.S. Over the last 12 months, Dayforce generated approximately $1.9 billion of revenue, including recurring revenue of about $1.4 billion.

As always, thank you for reading, and if you’ve enjoyed this, please consider sharing, liking, commenting or subscribing!

Disclosure: Of the stocks mentioned in this report, I am long Intuit and Paychex. This report is for informational purposes only and is not a recommendation to buy or sell any stock. Finally, while I rely on the information in this report to guide my investment decisions, you should not, because I cannot guarantee its accuracy.

HCM stands for human capital management

Great overview. Looking forward for more HCM deep dives

Great analysis! A couple other areas to look for in 'Revenue Model' category as a go forward/consolidation plays:

1. Employee financial services (banking/credit products for their networked employees > eg: their customers employees). Believe most offer this through partners today but could be potential growth opportunity given valuation of companies with consumer focus like Dave/Chime. Acquiring + servicing economics may be attractive

2. Business financial services. As you note there are different flavors of this strategy playing out between Paylocity acquisition of airbase, ADP/Fiserv, Paychex/BILL.

Intuit is certainly furthest along in executing against this octopus revenue approach but seems several companies are at a scale that could be accretive to someone encountering slower growth.