Shift4 Payments: Positioned to win in hospitality

But will success follow in newer verticals?

Shift4 Payments FOUR 0.00%↑ is No. 9 on My Top 10 Businesses in Payments and FinTech. As a reminder, this ranking is based on a fundamental assessment and does not consider valuation. Corpay CPAY 0.00%↑ was No. 10.

The Big Picture

Shift4 has grown leaps and bounds since its June 2020 IPO, with revenue1, volume2, and profit3 increasing over 4x, 6x, and 7x, respectively. New client wins, customer conversions from gateway services to end-to-end processing, acquisitions, and buyouts of residual commissions and distribution partners have contributed to the company’s outstanding results. At the time of its IPO, Shift4 was focused primarily on U.S. restaurants. Now, the company serves merchants in a number of verticals across the globe.

“But just to give some examples, we're in a majority of stadiums in the country. We weren't in a single one 4 years ago. We are in 40% of the hotels in the country. We weren't in a single one 8 years ago. And we're operating in over 50 countries today, and that's even before the acquisition of Global Blue, and we're operating in one country just about 18 months ago.”

Taylor Lauber, President of Shift4 Payments at the Barclays Emerging Payments and FinTech Forum on May 20, 2025

Raising the stakes, Shift4 recently announced the acquisition of Global Blue for $2.5 billion, its largest ever, as its founder and CEO departs to lead NASA. Despite its strong performance, concerns about the sustainability of Shift4’s acquisition-driven growth persist. The market prefers narrowly focused Payments companies that leverage homegrown cloud-based platforms to drive attractive organic growth. Shift4 doesn’t fit the mold, but its track record is hard to ignore.

Investment Thesis

Shift4 excels in hospitality and table-service restaurants with a clear right to win. I believe the company is less advantaged in other verticals, which form its Unified Commerce segment.

Shift4 wins in hospitality because it is uniquely capable of delivering a unified payments experience to the most complex businesses in the world, eliminating the need for multiple vendors, reducing the cost of payment acceptance, and most importantly, providing a consistent commerce experience for guests.

The company integrates its payments platform with more than 550 software companies, including nearly all the leading providers for hotels, resorts, sports and entertainment venues, and theme parks. Each new customer and software integration furthers the company’s advantage over competitors.

Despite making only two moderate acquisitions—VenueNext and Appetize for $176 million combined—I estimate Shift4’s hospitality volume grew to $49 billion in 2024, up from $13 billion in 2021.

In restaurants, Shift4 is no Toast, but they’re still pretty darn good. As Shift4 likes to say, SkyTab, its flagship point-of-sale system for restaurants, is one of only two cloud-based solutions optimized for table service that is being actively invested in and distributed at scale. Data supports this claim. Although Shift4 trails Toast, its volume has grown over twice as fast as the industry since 2021, indicating significant market share gains.

Acquisitions fuel Shift4’s cross-sell strategy. Beyond gaining complementary capabilities or entering international markets, Shift4 acquires merchants to cross-sell its end-to-end processing solution. Including the Global Blue acquisition, Shift4 sees a $1.4 trillion volume cross-sell opportunity. While not expecting to capture most of this volume, even a 5% success rate would boost Shift4’s 2024 end-to-end volume by 42%.

Source: Shift4 Payments Investor Day Presentation, February 18, 2025

Shift4's advantage in Unified Commerce is unclear. Since its IPO, Shift4 has spent $1.5 billion on acquisitions, with about half targeting verticals that comprise Unified Commerce and include online gaming, nonprofits, airlines, internet services, e-commerce, and retail. Retail and e-commerce offer significant opportunities but are highly competitive. Although not dismissing the potential for a competitive edge, I see less advantage for Shift4 in Unified Commerce than in hospitality and restaurants.

Company Overview

Shift4 offers three main solutions:

A payments platform supporting all major payment types with robust security.

A proprietary gateway integrating with over 550 hospitality-focused software companies.

Technology solutions, including SkyTab POS and Mobile for restaurants, SkyTab Venue for sports and entertainment, analytics, an e-commerce platform, and a marketplace for seamless third-party app integration.

Shift4 integrates its payment platform with its technology solutions and over 550 hospitality-focused software companies via its proprietary gateway. Some merchants using Shift4’s gateway choose another processor, which Shift4 supports. However, Shift4 has migrated a significant portion of this $180 billion opportunity (at the time of its IPO) to its end-to-end processing solution.

Go-To-Market

Shift4 uses a mix of partners and direct sales to distribute its solutions.

In restaurants, Shift4 relies on internal sales, support networks, independent software vendors, or ISVS, and value-added resellers, or VARs, to sell its processing solutions and point-of-sale systems, including SkyTab.

In hospitality, Shift4 leverages over 550 integrated hospitality-focused software companies and direct sales to sell its processing solutions.

For sports, entertainment, and Unified Commerce, Shift4 uses only direct sales.

For partner-sold solutions, Shift4 pays ongoing residual commissions based on processed volume.

Since its IPO, Shift4 spent nearly $400 million insourcing distribution, including $311 million to buy out residual commission streams and $82 million to acquire six software companies, converting their merchants to Shift4’s end-to-end processing solution. Partnership payments now account for less than 12% of revenue, down from over 21% at the IPO.

Source: Shift4 Payments Investor Day Presentation, February 18, 2025

Competition

Shift4 faces intense competition in providing payment and commerce services to merchants from legacy and pure-play processors like Adyen, Stripe, J.P. Morgan JPM 0.00%↑, Bank of America BAC 0.00%↑, Elavon, part of U.S. Bank USB 0.00%↑, Fiserv FI 0.00%↑, Worldpay and Global Payments GPN 0.00%↑, and commerce platforms such as Shopify SHOP 0.00%↑, Toast TOST 0.00%↑, Square XYZ 0.00%↑ and Lightspeed LSPD 0.00%↑.

In U.S. table-service restaurants, Shift4’s main competitor is Toast, but both are gaining market share from legacy providers NCR VYX 0.00%↑ and Oracle’s ORCL 0.00%↑ MICROS, as well as smaller independent software vendors.

Shift4’s 10-K identifies Elavon and FreedomPay as primary competitors for its proprietary hospitality gateway. While FreedomPay’s volume and revenue data is unknown, U.S. Bank reports Elavon’s performance. Since 2021, Elavon’s processed volume grew 27%, compared to an estimated 277% increase in Shift4’s hospitality volume. However, Elavon’s 2024 volume of $576 billion far exceeds Shift4’s estimated $49 billion, indicating Shift4 has room to capture more hospitality market share.

A Brief Company History

Jared Isaacman founded United Bank Card, the predecessor to Shift4 Payments, in 1999 at age 16.

United Bank Card differentiated itself by reducing merchant sign-up and onboarding time and offering free hardware.

Over the years, the company acquired several point-of-sale systems and payment gateways.

In 2020, Shift4 went public. Since then, it has completed $1.5 billion in acquisitions and established Unified Commerce, encompassing all verticals except restaurants and hospitality. In 2024, Unified Commerce accounted for 42% of the company’s volume.

In November 2023, Shift4 announced it was exploring strategic alternatives. Initially, Global Payments was said to have expressed interest in acquiring Shift4. Later, Reuters reported Fiserv and Amadeus were vying to buy the company. Ultimately, Shift4 rejected all offers, if they occurred, as insufficient.

In December 2024, President Donald Trump announced Jared Isaacman as his pick for NASA's next administrator. Shift4 shares dropped over 12% that day.

On February 18, 2025, Shift4 announced the acquisition of Global Blue for $2.5 billion, alongside its Q4 2024 results, 2025 guidance and Investor Day. Global Blue enables tax-free cross-border shopping for affluent consumers at luxury brands.

Risks

Shift4 faces the following risks:

Nearly 60% of the company’s volume comes from restaurants and hospitality, including hotels, resorts, sports, entertainment, and theme parks, where consumer spending is discretionary. Though historically resilient during economic downturns, the company may experience slower growth or decline in the next recession as it matures.

Founder and CEO Jared Isaacman plans to depart as the company completes its largest acquisition, posing significant execution risks.

Shift4 relies on acquisitions to drive growth and enhance its cross-sell funnel. Failure to find attractive acquisition opportunities could slow Shift4's growth.

After acquiring Global Blue, Shift4 expects its gross leverage to reach 4.7x, potentially limiting more attractive acquisition or share repurchase opportunities as it deleverages.

Most of the company's recent acquisitions are outside its core restaurant and hospitality sectors. It is unclear what advantage, if any, Shift4 has over competitors in these markets.

Financial Review

Revenue

Shift4 presents Gross Revenue Less Network Fees (GRLNF) as its non-GAAP revenue measure. GRLNF comprises two main components:

end-to-end processing fees and

subscription and other revenues, including SaaS-based fees for POS systems and its analytics platform, hardware sales, and software license sales.

Fees for gateway services make up a small percentage of Shift4’s GRLNF.

In 2024, Shift4’s spread4 was 61 bps, down from 78 bps in 2019.

One reason for the decline is a reduced mix of restaurant volume, which has the highest spreads, partly due to their smaller average merchant size.

Source: Shift4 Payments Q1 2025 Presentation, April 29, 2025

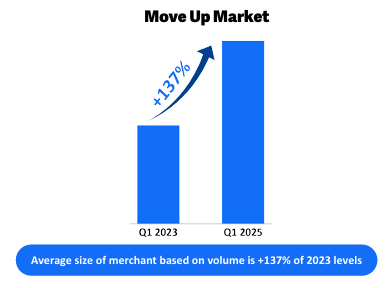

Similarly, Shift4’s newer verticals have larger average merchant sizes, supporting the company’s move upmarket.

Source: Shift4 Payments Q1 2025 Presentation, April 29, 2025

Profitability

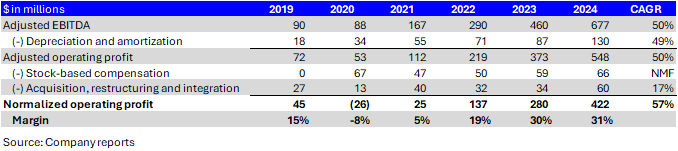

In 2024, Shift4's normalized operating profit was $422 million, 31% of GRNLF, up 16 points since 2019. Leveraging fixed costs over a larger volume base and in-sourcing distribution contributed to the expansion.

Investment Checklist

Below is an evaluation of Shift4 using my Investing Checklist.

Disclosure. Shift4 provides adequate disclosure for fair value determination, reporting key performance indicators like end-to-end processing volume and blended spreads. More consistent disclosure of processing volume composition and merchant numbers would be preferable. Shift4’s adjusted earnings include all “special” items—stock-based compensation, amortization of acquired intangibles, restructuring, acquisition-related expenses, gains, losses, and asset impairments—using the most generous earnings definition, which is not the best practice.

Growth. Shift4 often acquires businesses but sustains strong organic growth. For 2025, the company anticipates GRLNF to rise over 20% on an organic basis, following a 26% increase during 2024. Shift4 serves many small business customers, with no single customer significantly impacting revenue. Growth stems solely from increased volume, not pricing.

Profitability. In 2024, Shift4's normalized operating profit5 was $422 million, 31% of GRNLF, up 16 points since 2019. Leveraging fixed costs over a larger volume base and in-sourcing distribution contributed to the expansion. In the last five years, Shift4 added back $178 million in restructuring, acquisition, and integration costs to arrive at its adjusted EBITDA measure.

Free Cash Flow. Shift4 generated free cash flow of $708 million over the last three years, more than 100% of my normalized net profit6 calculation. Stock-based compensation represents about 5% of GRLNF.

Financial Health. Shift4’s total debt-to-EBITDA is expected to reach 4.7x on a pro-forma basis at the close of the Global Blue acquisition, on the high side, and potentially limiting more attractive acquisition or share repurchase opportunities as it deleverages.

Source: Shift4 Payments Investor Day Presentation, February 18, 2025

Returns. Shift4's return on average tangible assets was 28% over the past twelve months. Return on average capital was 10%.

Capital Allocation. Shift4’s primary use of excess capital is acquisitions. Since its IPO, Shift4 has spent $1.5 billion on acquisitions, strengthening its restaurant and hospitality presence, expanding globally, and opening new verticals in its Unified Commerce division.

The company spent $315 million on buying out residual commission streams and $457 million on share repurchases since 2020.

Disclosure: I am long Shift4 Payments, Global Payments and Fiserv. I do not hold a position in any other stock mentioned in this article. This article is for informational purposes only and is not a recommendation to buy or sell Shift4 Payments or any other stock.

Gross revenue less network fees

End-to-end processing volume

Adjusted EBITDA

Spread equals end-to-end processing fees as a percentage of end-to-end payment volume

Here is how I define normalized operating profit:

GAAP operating profit + amortization of acquired intangible assets

I do not add back:

Stock-based compensation

Restructuring or

Acquisition-related expenses

Net profit does not add back stock-based compensation, legal, merger, integration, and restructuring costs